For many Indian families, sending a child abroad for higher education is a dream built over the years. A degree from the United States, the United Kingdom, or Canada is often seen as a pathway to global exposure, better career opportunities, and long-term financial security. But in recent years, this dream has become far more expensive.

In our earlier analyses, we looked at how education inflation is rising steadily within India across school education, undergraduate, and postgraduate programs. The trend is now visible globally as well. International education today involves much more than tuition fees. Families are facing rising living costs, a weaker rupee, and higher upfront financial requirements.

In this edition, we look at how the overall cost of studying in the U.S., UK, and Canada has changed, and why education inflation abroad is becoming a major planning challenge for Indian families.

| Key Takeaways |

|

|

|

How The Three Countries Compare

When it comes to international education, the total cost can vary significantly depending on the country and the course chosen.

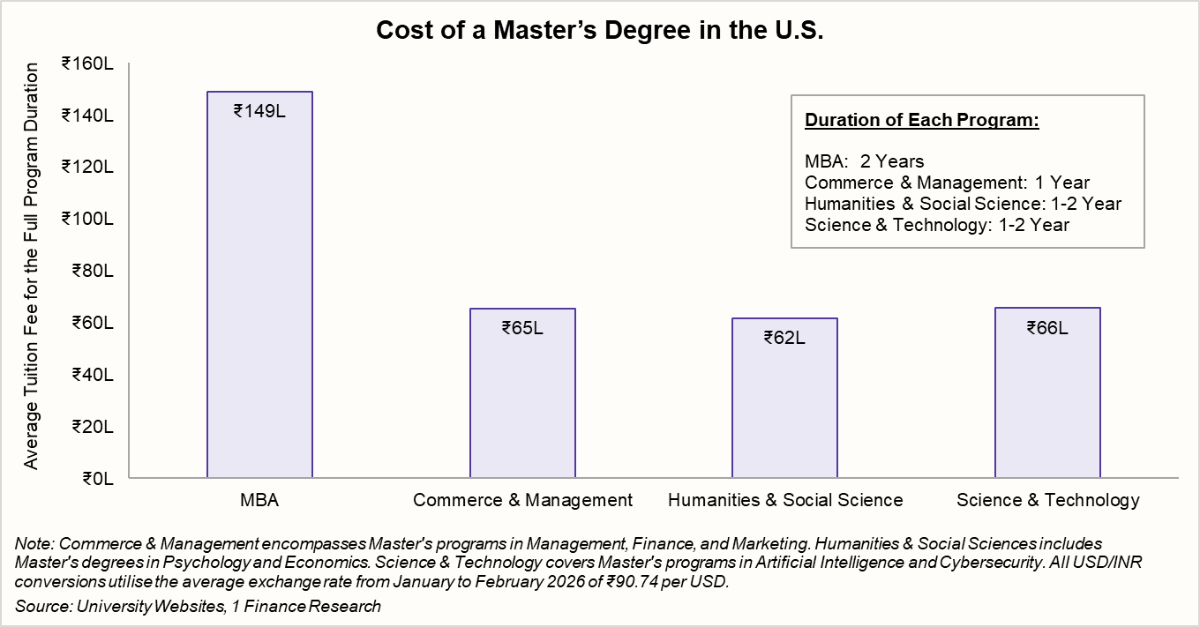

The U.S. continues to be the most expensive destination among the three. Tuition alone for an MBA can touch nearly ₹1.5 crore, while programs in science, management, and humanities typically fall in the ₹62-66 lakh range. And this is only the academic cost. Living expenses, insurance, and other essentials can add significantly to the total outlay.

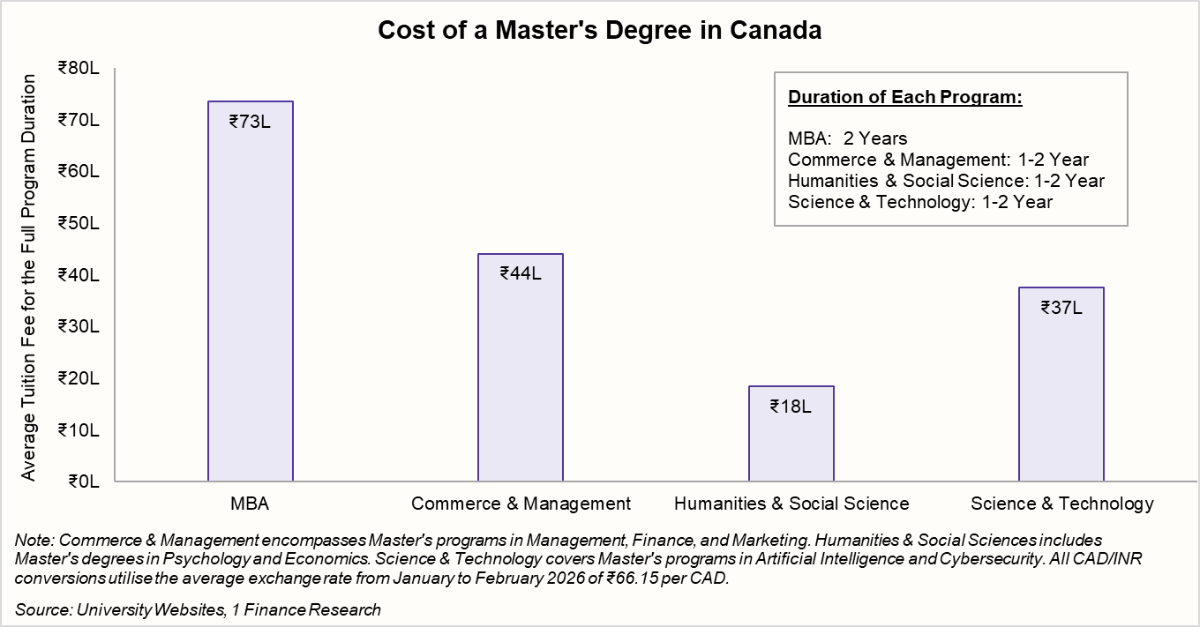

Canada is often seen as a more affordable alternative, but the gap is not as wide as it once was. MBA tuition is around ₹73 lakh, while other programs range between ₹18-44 lakh, depending on the field. However, rising housing costs in major student cities have pushed overall expenses higher in recent years.

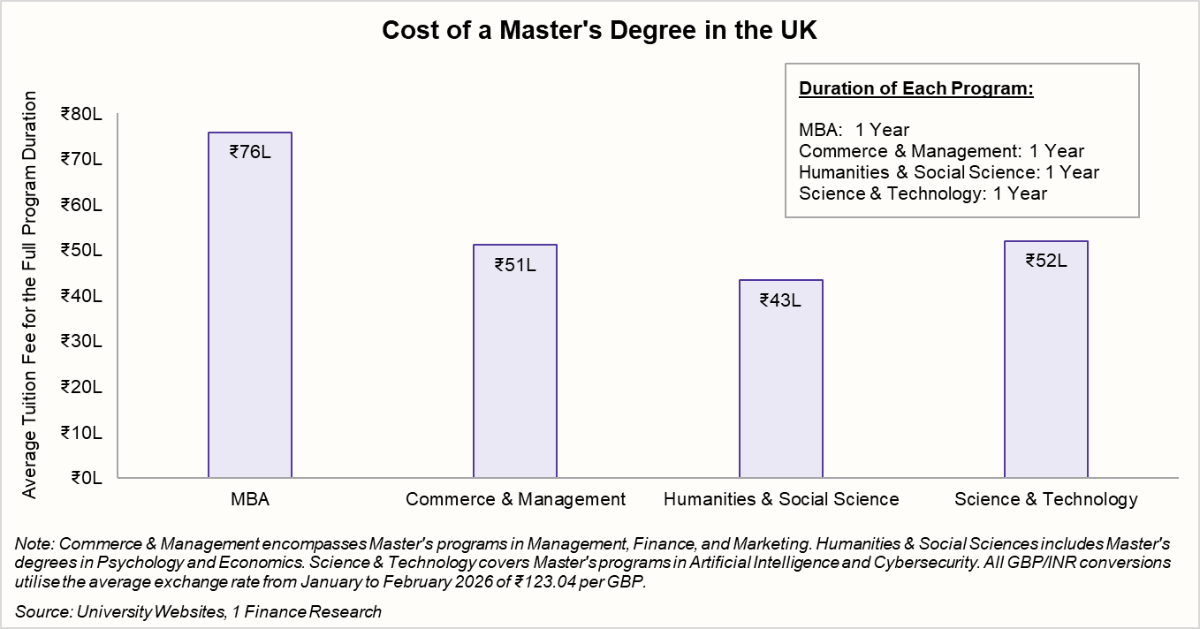

The UK sits between the two. MBA programs cost about ₹76 lakh, and most other master’s degrees fall in the ₹43-52 lakh range. The key advantage is duration. Many UK master’s programs are completed in one year, which helps reduce both tuition and living costs.

The differences across countries highlight an important shift. Choosing where to study is no longer just about rankings or career prospects. It is equally about understanding the total financial commitment and selecting a destination that aligns with the family’s long-term financial plan.

Recommended for you

Readers also explored

India’s Unemployment Rate in 2025

Nifty 50 Companies List 2025 : Top 50 Stocks in India

It is Not Just Tuition Anymore

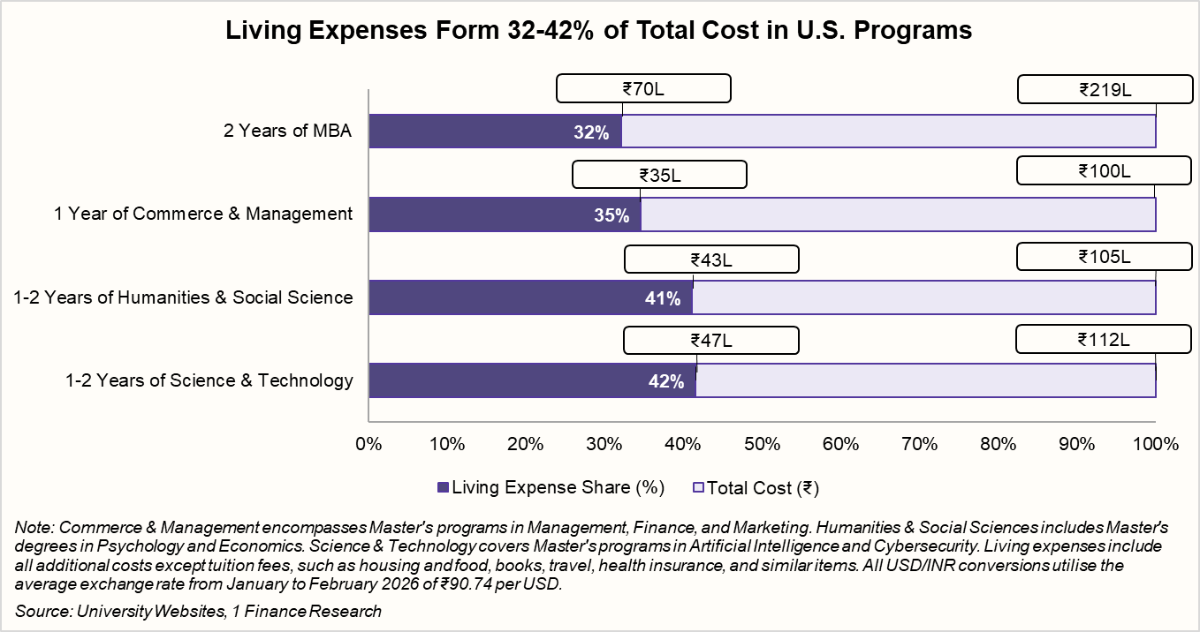

When families think about the cost of studying abroad, tuition is usually the first number they look at. But the reality is that living expenses now account for a large share of the total cost and, in some cases, nearly half of the overall budget.

In the U.S., living expenses account for about 32-42% of the total program cost. For a two-year MBA, this amounts to nearly ₹70 lakh spent solely on accommodation, food, insurance, and daily living expenses. Even for shorter programs, students may spend ₹35-47 lakh outside of tuition.

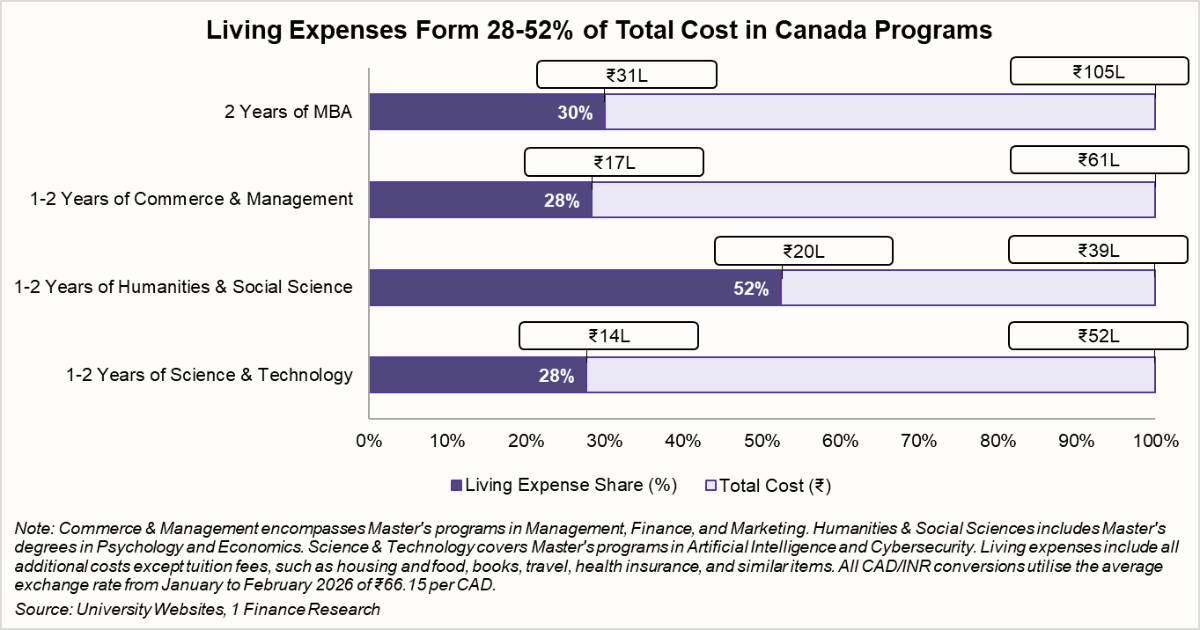

In Canada, the variation is even wider. Living costs form 28-52% of the total expense, depending on the course. For some humanities programs, more than half of the total cost goes toward rent and daily living, highlighting how housing pressures in cities like Toronto and Vancouver are reshaping the overall budget.

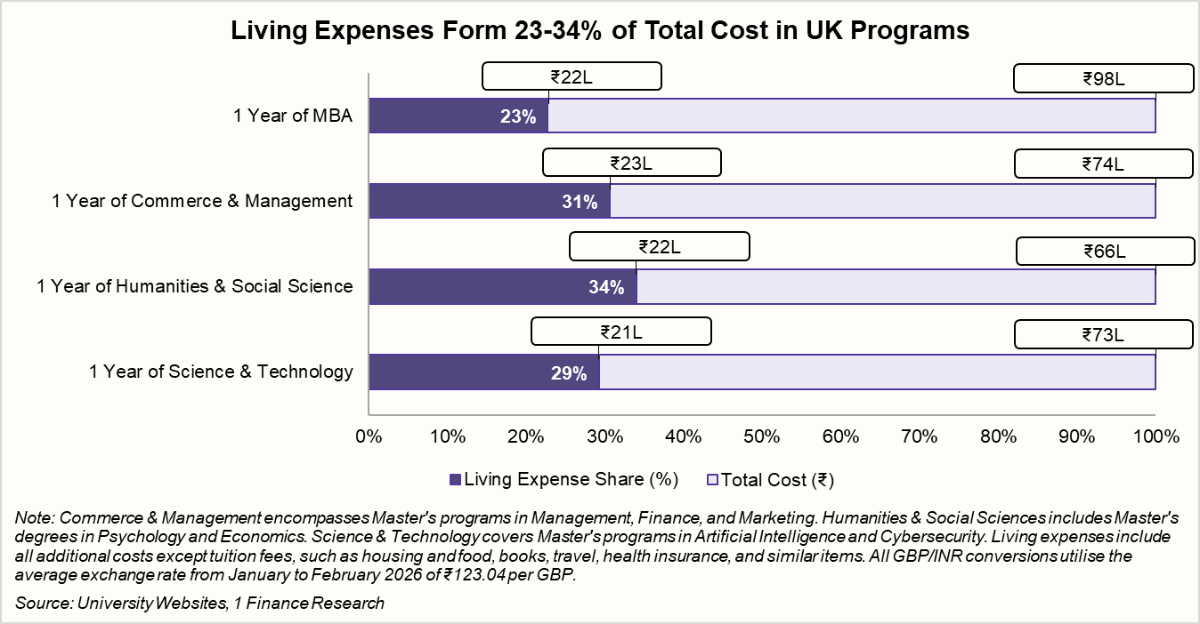

The UK appears relatively lower at 23-34%, largely because most master’s programs are completed in one year. Even then, students typically spend ₹21-23 lakh on living costs alone.

The takeaway is clear. Tuition is only one part of the equation. Rising rents, higher food and transport costs, and mandatory health insurance mean that the day-to-day cost of living has become one of the biggest drivers of education inflation abroad. For families planning overseas education, budgeting for lifestyle costs is now just as important as planning for university fees.

💡A hidden cost pressure families often miss

Most countries now require students to show proof of funds before issuing a visa. This includes the ability to cover tuition, living expenses, and an additional buffer for healthcare and emergencies. For families, this means arranging a large pool of liquid savings even before the student leaves India. |

When Fee Hikes Meet Currency Depreciation

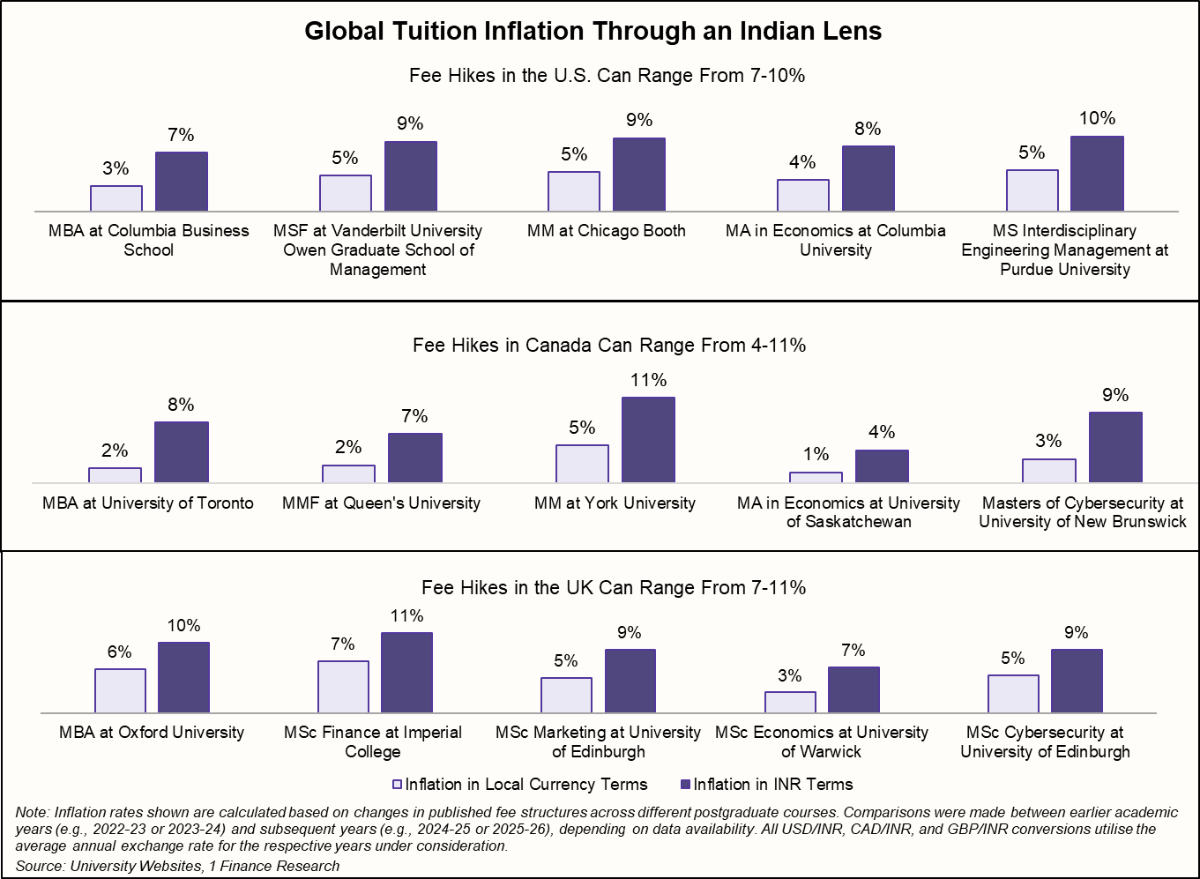

Tuition fees at leading universities in the US, UK, and Canada have been rising steadily, reflecting the broader global trend of education inflation. In local currency terms, annual fee increases typically range between 2-7%, depending on the course and institution. While these increases may appear manageable at first glance, the experience for Indian families is very different.

Once rupee depreciation is factored in, the effective increase in costs rises sharply to 7-11% in rupee terms. In other words, even a modest fee hike abroad can translate into a much larger jump in the actual amount families have to pay.

This dual pressure of rising global tuition and a weaker rupee means that the real cost of international education is increasing much faster than headline numbers suggest. Over the course of a one or two-year program, this combined effect can add several lakhs to the total expense, making currency movements just as important as tuition trends in overall education planning.

Why Early Planning Matters More Than Ever

The cost of international education is rising steadily, driven by both global fee increases and currency movements. For Indian families, the effective cost typically rises by 7-11% annually in rupee terms, and total expenses go well beyond tuition to include living, insurance, and travel. Planning ahead helps avoid last-minute financial stress.

How to plan effectively

- Assume 10-12% annual cost inflation as a realistic baseline for overseas education.

- Build a buffer for currency risk, as rupee depreciation can significantly increase the final cost.

- Plan for the full expense, including living costs, health insurance, travel, and other essentials, not just tuition.

- Start building the education corpus early to reduce dependence on high-cost education loans.

- Review the plan every 2-3 years to account for fee changes, exchange rate movements, and evolving course or country preferences.

Families need to start saving early, build a cushion for currency fluctuations and annual cost increases, and plan for the full cost rather than just tuition. It is also important to evaluate the return on investment based on the course, university, and employment prospects after graduation.