The past few weeks have been decisive for the Indian economy. At its latest Monetary Policy Committee meeting, the Reserve Bank of India did more than hold rates steady; it quietly shifted the focus of policy. The repo rate was left unchanged at 5.25%, but the real action was elsewhere.

The VRR investment cap has been scrapped, and banks may be allowed to lend to REITs. The former is expected to support foreign participation in debt markets and help anchor bond yields, while the latter could improve funding access for REITs and strengthen the broader real estate ecosystem.

At the same time, India is transitioning to a new inflation series, a technical shift that could reshape how we interpret price trends in the coming quarters. This edition focuses on what truly moves portfolios from here: rates, inflation, liquidity, and growth.

Liquidity, Transmission, and the RBI’s “Wait and Watch” Approach

The Reserve Bank kept the repo rate unchanged at 5.25%, signalling a temporary pause rather than a rush into fresh cuts. Inflation is running below the 4% target (CPI projected around 2.1% for FY26), while GDP growth is forecast at about 7.4%, putting the economy in a “Goldilocks” zone, with strong growth and low inflation.

Yet the latest MPC outcome makes one thing clear: the RBI’s priority has shifted from cutting rates to strengthening liquidity and improving transmission.

Why no rate cut this time?

The decision to pause was not driven by inflation concerns. Instead, the RBI appears cautious about the effectiveness of any further easing in the current environment. Two constraints stand out.

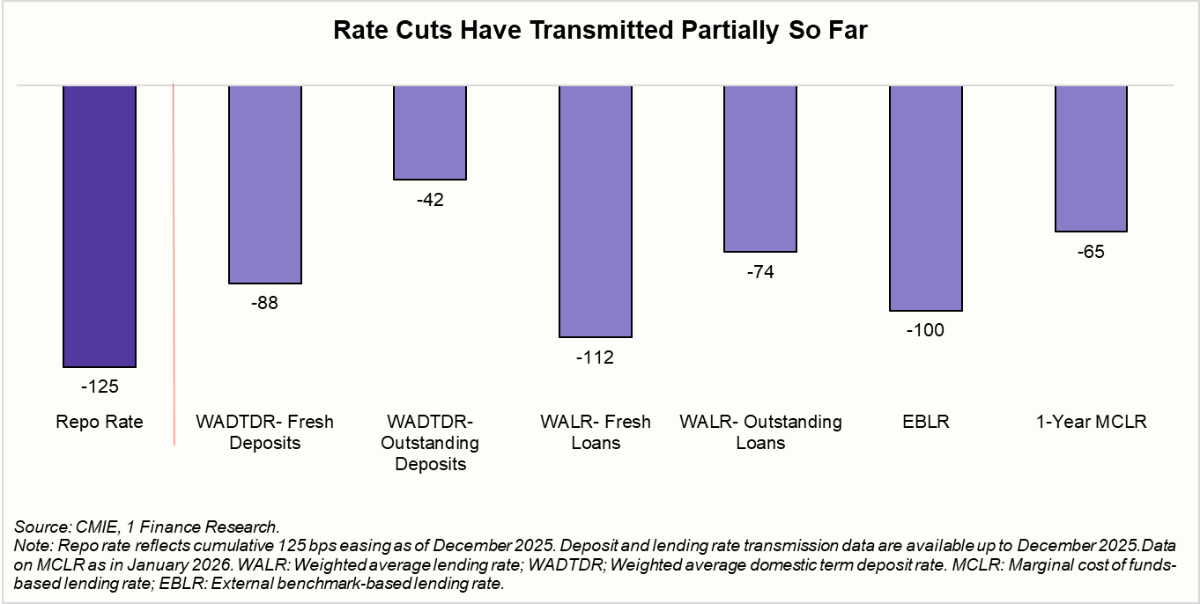

First, transmission is still incomplete. While policy rates have moved earlier in the cycle, lending rates, especially in fixed-rate segments and older loan books, have adjusted only gradually. For many borrowers, the benefit of past policy moves has yet to fully pass through.

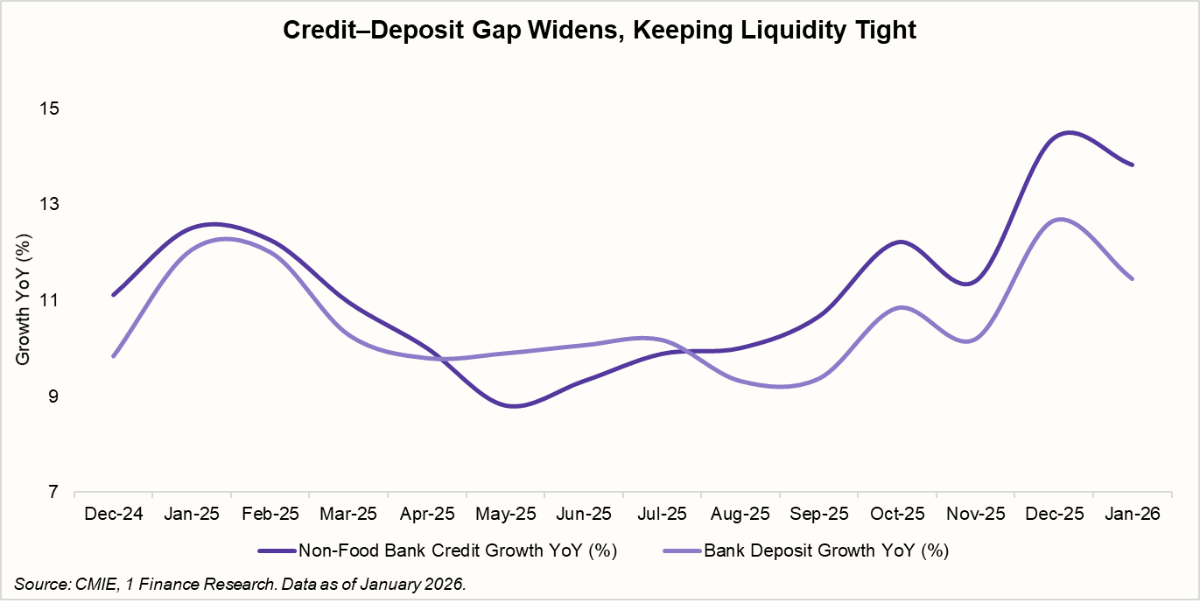

Second, liquidity remains uneven. Credit growth has been running ahead of deposit growth, widening the credit-deposit gap. This has kept system liquidity tight at the margin and increased banks’ reliance on market borrowing. In such an environment, a rate cut would not translate effectively into lower lending rates and could even intensify funding pressures.

Put simply, cutting rates before liquidity eases and transmission improves would have limited real-economy impact. That’s why the RBI is currently focused on strengthening the banking system liquidity and improving financial conditions, rather than easing the policy rate itself.

Recommended for you

Readers also explored

Balancing Slowdowns and Sectoral Strength

Currency in Circulation: How Much Money Exists in the World?

Major MPC‑Feb‑2026 announcements at a glance

Let’s look at some of the major announcements made by the RBI in the latest MPC meeting:

| Announcement | What It Means | Impact For Advisors & Investors |

|---|---|---|

| VRR investment cap scrapped (Rs 2.5 lakh crore) | FPIs can now invest in Indian bonds under VRR (Voluntary Retention Route) without the earlier ceiling, within overall FPI limits. | ▲ FPI flows ▲ 10-yr G-Secs & high-grade corporate bonds ▼ Yield volatility |

| Banks may lend to REITs (proposal) | Banks may be permitted to extend loans to REITs under prudential safeguards, improving access to funding for the sector. | ▲ REIT funding access ▲ Cash-flow visibility ▲ Distribution stability |

| MSME collateral-free loan limit doubled to ₹20 lakh | Easier access to credit for micro and small businesses without additional collateral requirements. | ▲ MSME credit growth ▲ Business activity ▲ MSME-linked credit products and regional banks/NBFCs |

| Digital-fraud compensation framework (up to ₹25,000) | Proposed customer protection norms for small-value digital fraud losses aim to strengthen trust in digital transactions. | ▲ Trust in digital transactions ▲ UPI & digital banking adoption ▲ Online investment usage |

The latest policy should not be read as inaction. The RBI is using this phase to fix the conditions that make rate cuts effective by easing liquidity constraints, improving funding visibility for banks, and allowing transmission to catch up.

The next shift in the policy narrative will depend not just on liquidity and growth, but on how inflation itself evolves and how it is measured.

That brings us to the next important development: India’s transition to a new CPI base, a technical change that could influence how inflation trends and future rate expectations are interpreted in the months ahead.

The Inflation Shift Between 2012 and 2024

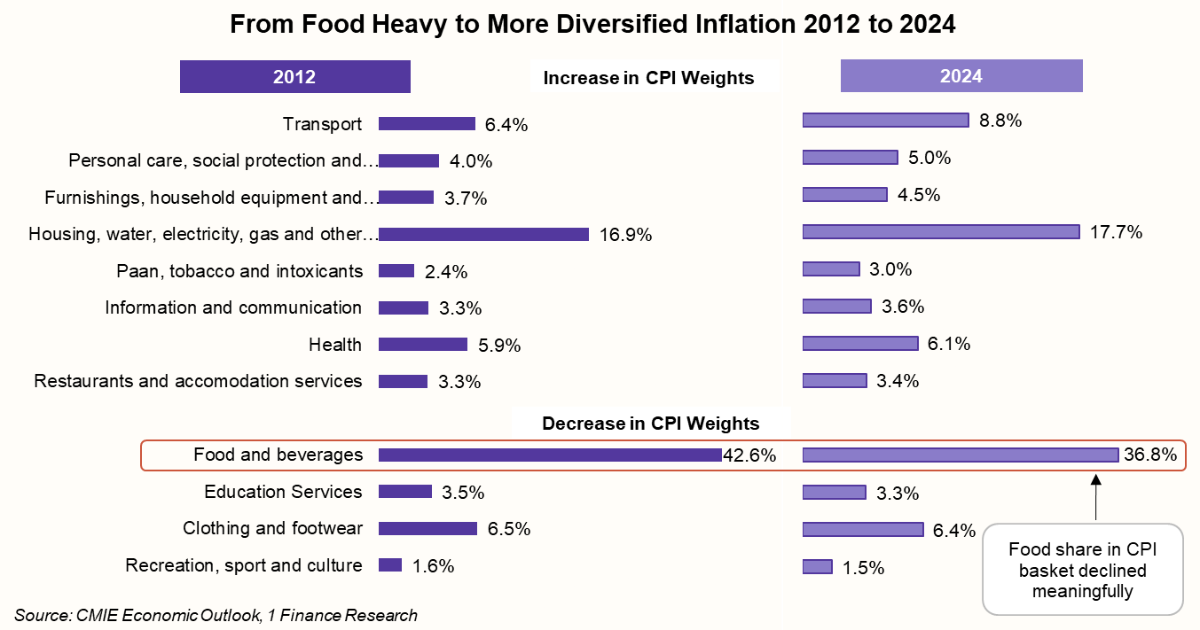

The way we measure prices just got a long-overdue upgrade. MoSPI has shifted the inflation base year from 2012 to 2024. This captures how India actually spends today.

The old basket stuck to habits from over a decade ago. It loaded up on basic staples and skipped the digital economy. Today, India spends more on data, travel, and health than it did in 2012.

The new series draws from the 2023-24 Household Consumption Survey. It better represents today’s consumption patterns, reflecting a more modern and aspirational India. It moves away from the earlier food-heavy structure toward a more balanced and realistic consumption basket.

Broader Coverage, Deeper Representation

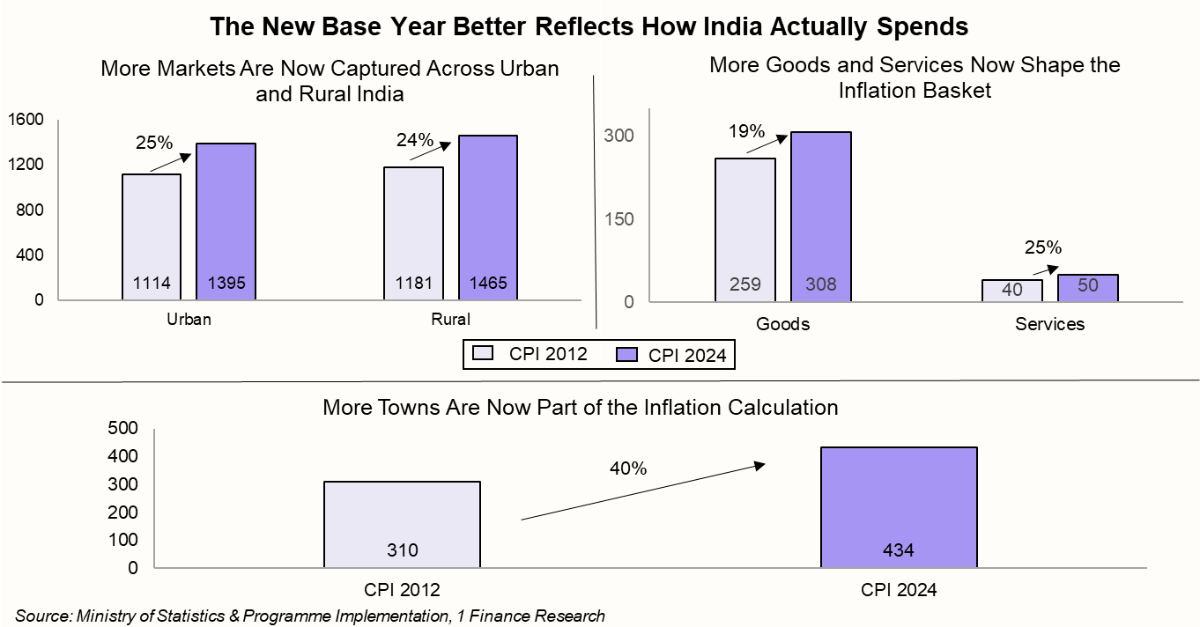

The coverage has also expanded across the country. The new index tracks 358 items, up from 299 in the previous series. It now includes items like streaming services, gym equipment, and babysitters.

This reset also means better coverage of 1,465 rural and 1,395 urban markets (with urban including 12 additional online markets capturing e-commerce prices weekly in large cities). For the first time, rural house rent is officially part of the calculation. This makes the index far more representative of the entire population.

What This Means for Our View on Inflation and Repo Rate

With the shift to the 2024 base year, we rebuilt our inflation forecasts. The direction remains unchanged, but the path evolves.

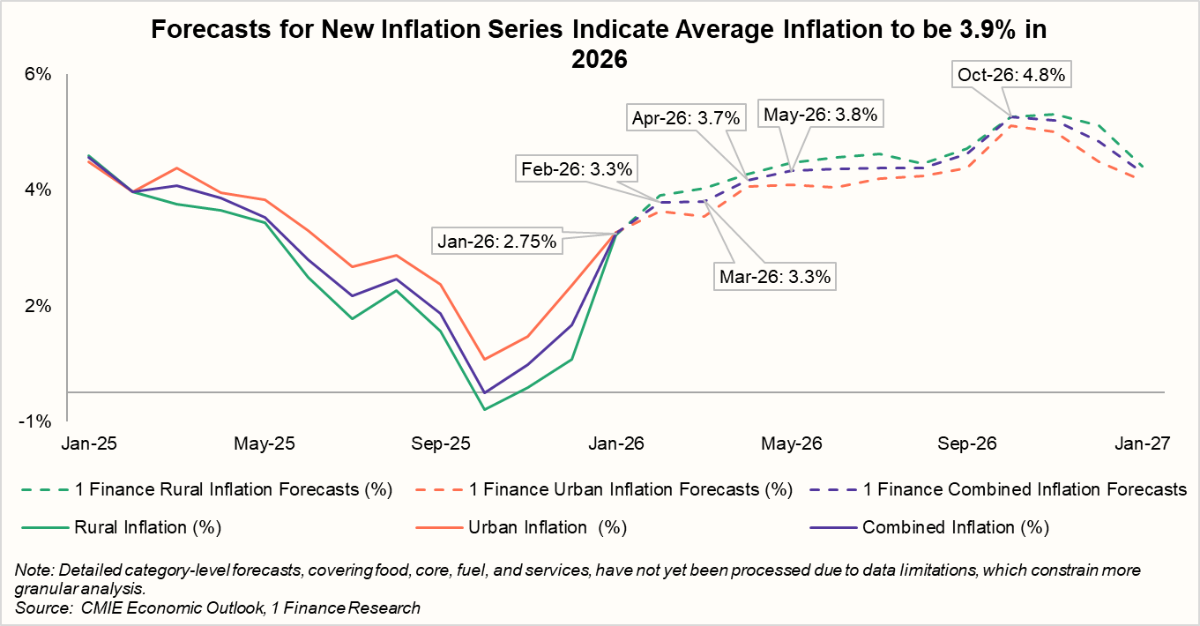

Inflation is expected to rise in 2026. It increased to 2.7% in January 2026, partly due to a favourable base effect, and is likely to edge higher gradually as the year progresses. Overall, average inflation for 2026 is projected at 3.9%, with further increase expected in the later months, potentially reaching around 4.8% by October 2026.

Rural inflation remained lower than urban inflation in 2025, reflecting the strong role of food prices and seasonal factors. As these effects fade, both rural and urban inflation are projected to increase, pushing overall inflation higher towards the end of 2026.

With inflation expected to stay below the 4% target through much of 2026, and the stance remaining neutral, policy settings provide flexibility for gradual rate cuts if growth momentum warrants support.

Under our Taylor Rule framework, we see scope for 50-75 bps rate cuts by the end of 2026, conditional on a normal monsoon that keeps the food inflation in control and stable global crude oil prices, thereby limiting imported inflation and excessive rupee depreciation.

| Scenario | Probability | Favourable Triggers |

|---|---|---|

| No rate cuts (Repo: 5.25%) | 5% | If the inflation spikes rapidly and the INR depreciates further, it will restrict the RBI’s moves. Unlikely. |

| Modest easing: 25 bps (Repo: 5%) | 20% | Inflation reaches the 4% target. Domestic growth remains strong, and the RBI prefers to preserve policy space. |

| Base Case: 50 bps (Repo: 4.75%) | 40% | Base case scenario. Most likely. Inflation remains benign, and the domestic and external conditions remain stable |

| Deep easing: 75 bps (Repo: 4.5%) | 30% | Inflation persists below 3%. Global growth slows down, and domestic demand signals appear weak, prompting the RBI to cut rates. |

| Aggressive easing: 100 bps (Repo: 4.25%) | 5% | Exceptional downside: Domestic growth drops, deflation persists or a major global shock forces a massive easing. Unlikely. |

Conclusion

At the recent MPC meeting, there was no rate cut. But that does not mean there was no action. In fact, some of the most important developments were structural.

First, the scrapping of the VRR investment cap. This removes the earlier ₹2.5 lakh crore ceiling and allows FPIs to participate more freely in Indian debt markets within overall limits. This will lead to improved foreign participation in bonds and reduce yield volatility over time. Second, the proposal to allow banks to lend to REITs. This strengthens funding access and improves cash-flow visibility for the real estate ecosystem.

Third, the new CPI base year reset. This aligns India’s inflation measurement more closely with today’s consumption patterns and with global standards. It improves credibility and makes future policy interpretation more meaningful. Based on our inflation forecasts using the new series, we still see room for calibrated rate cuts. That matters. Because the rate direction from here has implications for both Indian equity and debt markets.