Japan has emerged as one of the standout investment stories of 2026. By the end of June, the Nikkei-225 had gained around 39%, while the broader TOPIX advanced over 17%, comfortably outperforming the S&P 500 and other developed market peers.. Such sustained outperformance is particularly striking for an economy that, until recently, was better known for decades of deflation, ageing demographics and subdued growth.

The explanation lies beyond headline GDP numbers. Japan is undergoing a broader structural transition, where improving macroeconomic conditions, stronger corporate earnings and far-reaching corporate governance reforms are reinforcing one another. Together, these shifts are reshaping investor perceptions, improving corporate profitability and laying the foundations for a more durable market re-rating.

This blog examines how these three structural drivers have transformed Japan's economy and equity markets, and why the country's investment story looks fundamentally different from previous recoveries.

| Section | Key Takeaways |

|---|---|

| Macro Shifts Driving Japan's Economy in Recent Years |

|

| Japan's Equity Market Resurgence and Performance |

|

| The Third Driver of Japan's Equity Resurgence |

|

Macro Shifts Driving Japan's Economy in Recent Years

Following the change in political leadership in late 2025, ‘Sanaenomics’ has emerged as Japan's new economic agenda, centred on raising wages, strengthening domestic demand, encouraging private investment and lifting productivity. The objective is to shift the economy from decades of low growth towards a more self-sustaining expansion driven by domestic activity.

The reforms address one of Japan's biggest structural challenges. As nearly three in ten individuals are aged 65 or above and the working-age population continues to decline, future economic growth will increasingly rely on productivity gains and business investment instead of labour force expansion.

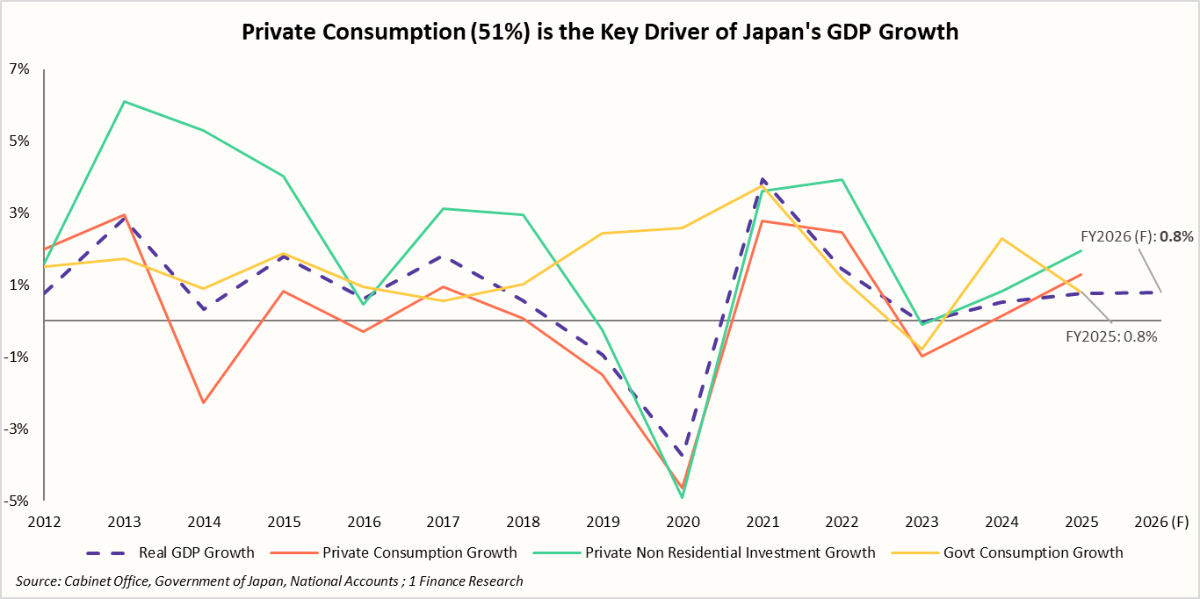

Private non-residential investment remained the strongest demand component, growing 2.3% in FY2025 (Japan's fiscal year ending Mar-26), supported by capital expenditure in automation, semiconductors and AI. Private consumption rose 1.3%, while government consumption increased 0.8%. However, real GDP expanded by ~0.8%, as weak residential investment and softer external demand weighed on overall growth.

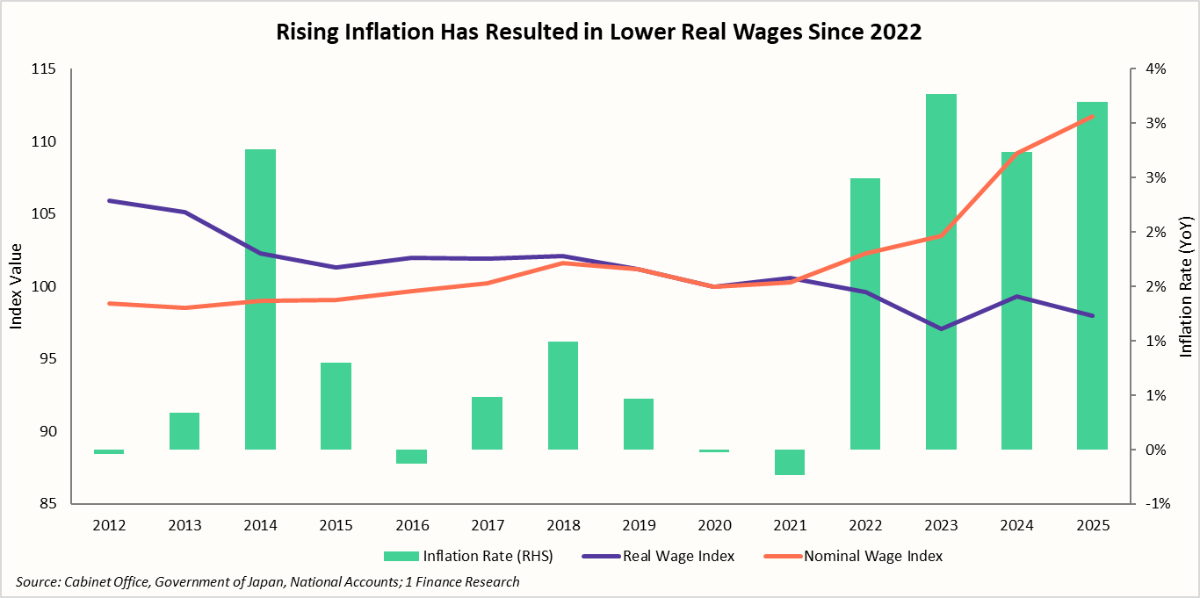

On the inflation side, Japan's macroeconomic landscape has changed markedly since FY2022. After nearly three decades of low inflation and intermittent deflation, consumer prices have consistently remained above the Bank of Japan's 2% target, driven initially by imported energy and food costs before broadening into domestic price pressures.

As the chart shows, inflation outpaced wage growth between FY2022-25, pushing real wages lower. Although Japan's annual Shunto wage negotiations between employers and labour unions delivered the strongest pay hikes in decades, higher inflation eroded much of the gains, weighing on household purchasing power and private consumption.

More recently, the outlook has begun to improve. Wage settlements and labour shortages are supporting faster nominal income growth. If wages continue to outpace inflation, Japan could move closer to a sustainable wage-price cycle, where higher incomes boost household spending, encouraging businesses to invest, hire and raise wages further.

Recommended for you

Readers also explored

India's IT Sector Outlook for FY2026

World GDP Breakdown 2025: Who Powers the Global Economy?

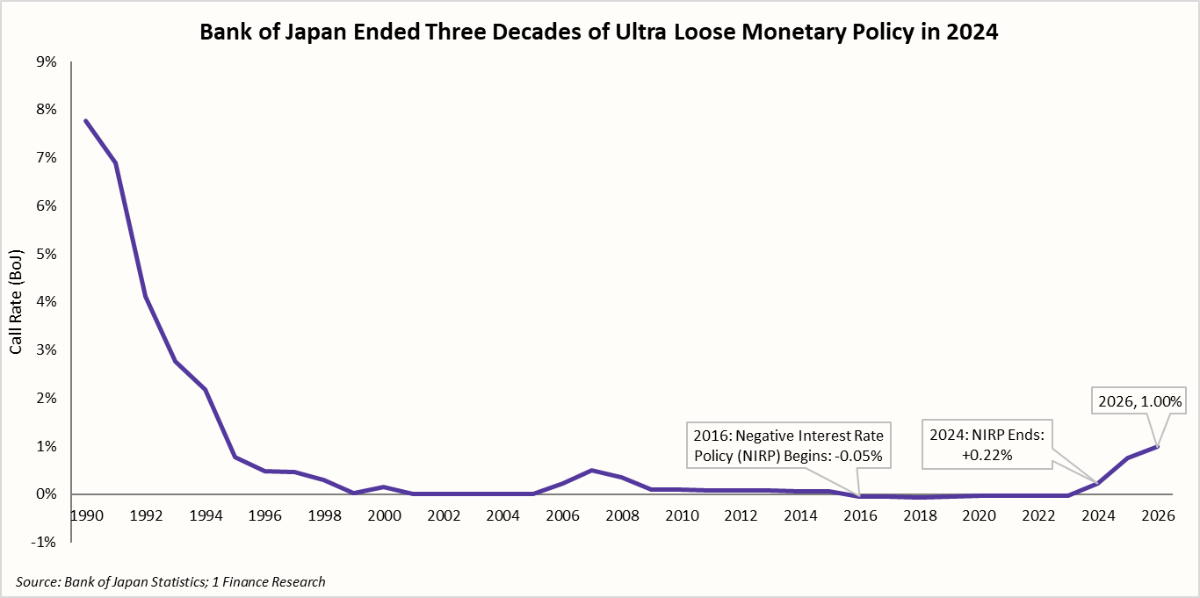

The Bank of Japan has complemented this transition by normalising monetary policy, raising its policy rate from -0.1% (Mar-24) gradually to 1.0% (Jun-26), ending nearly three decades of ultra-loose monetary policy. This shift reflects growing confidence that inflation is becoming more durable, supported by stronger wage growth and improving domestic demand rather than temporary price shocks.

With inflation remaining above target and wage growth strengthening, further gradual rate hikes over the next 12-18 months also remain likely, marking Japan's first sustained positive interest-rate cycle in more than three decades.

The return to positive interest rates marks a fundamental shift in Japan's macroeconomic landscape. While economic growth is likely to remain moderate, the quality of growth is improving, with stronger consumer spending, business investment and corporate pricing power providing a firmer foundation for sustained expansion.

For investors, this transition supports stronger corporate earnings, higher capital expenditure and better return expectations, helping explain why Japanese equities have re-emerged as one of the most attractive developed markets in 2026.

The next section examines Japan's two major equity indices, their historical performance and the sectors driving the market's resurgence.

Why Japanese Equities Are Outperforming Again

Financial markets often anticipate economic turning points well before they appear in headline GDP figures, and Japan has been no exception. As inflation returned, corporate earnings strengthened and domestic demand improved, investors began reassessing a market that had long traded at a discount to its global peers.

We evaluate Japan's equity market using two major benchmark indices, the Nikkei-225 and TOPIX. While the Nikkei-225 is more concentrated and tilted towards globally competitive exporters, TOPIX has broader market coverage with greater exposure to domestically oriented sectors such as financials, industrials and real estate. These structural differences often lead to distinct performance across market cycles, as summarised in the table below.

| Feature | Nikkei-225 | TOPIX |

|---|---|---|

| Methodology | Price-weighted | Free-float market cap weighted |

| Constituents | 225 large companies | 1,650 listed companies |

| Market Representation | Blue-chip leaders | Broad Japanese equity market |

| Sectoral Composition | Higher exposure to Technology (57%), Consumer Goods (20%) and Materials (13%) sectors. | Evenly Distributed across Electrical Appliances (22%), Financials (11%), Industrials, Real Estate and domestic sectors |

| Performance Profile | More cyclical and volatile | Broader and relatively steadier |

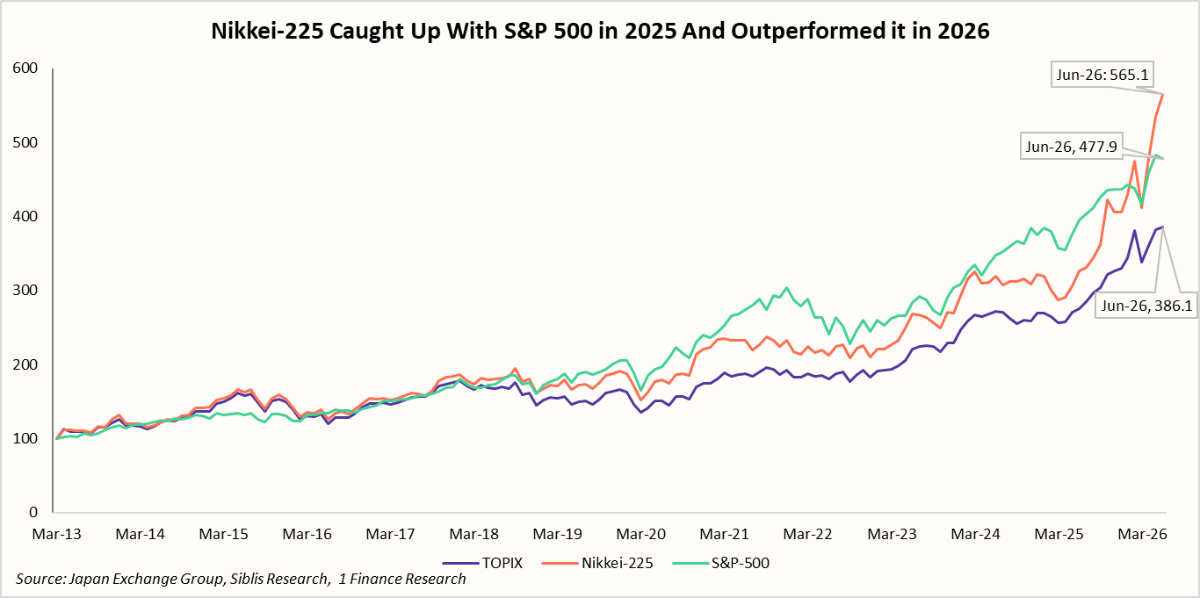

The contrasting characteristics of the Nikkei-225 and TOPIX are also reflected in their long-term performance. To place their returns in a global context, the chart below compares both indices with the S&P 500, the leading benchmark for developed equity markets. All three indices are rebased to 100 in Mar-13 and shown in local currency terms, isolating equity market performance. By Jun-26, the Nikkei-225 had risen to 565, compared with 478 for the S&P-500 and 386 for the TOPIX.

The chart also highlights a notable shift in market leadership. The S&P 500 has dominated for much of the past decade, driven by large-cap technology stocks. However, the gap between the three indices narrowed sharply in 2025, and by Feb-26 the Nikkei-225 had overtaken the S&P 500, reflecting stronger earnings, improving corporate fundamentals and renewed investor confidence in Japan's export-oriented companies.

The shift has widened in 2026. As of 30-Jun-26, the Nikkei-225 has gained 39.2%, comfortably outperforming both TOPIX (17.2%) and the S&P 500 (9.6%), reflecting renewed investor confidence in Japan's export-oriented market leaders and improving corporate fundamentals.

TOPIX (13-year CAGR: 10.2%), despite generating comparatively lower returns, has delivered a steadier and more broad-based advance, indicating that the recovery spread beyond a handful of large-cap companies to the wider Japanese market. As a result, it remains a more representative barometer of the country's overall corporate health.

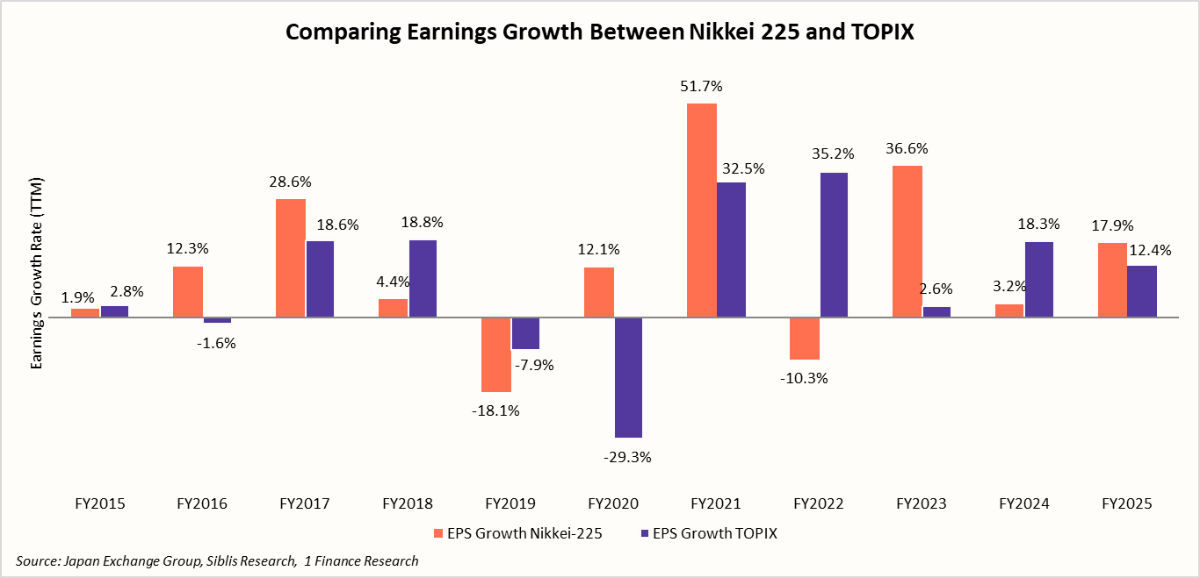

Market performance is ultimately driven by corporate earnings. The recent outperformance by Japanese equities has been supported not only by improving macroeconomic conditions but also by a strong recovery in corporate earnings.

The earnings recovery has differed across the two indices. The Nikkei-225 has delivered stronger but more cyclical earnings growth, while TOPIX has posted a steadier recovery. Most recently, TOPIX (18.3%) outpaced the Nikkei in FY2024 (3.2%), while both indices recorded double-digit earnings growth in FY2025, with TOPIX at 12.4% and the Nikkei-225 at 17.9%.

The recovery has been supported by a combination of cyclical and structural factors. A weaker Yen boosted the competitiveness and overseas earnings of exporters, while stronger pricing power, stable global demand and improving domestic consumption and investment strengthened profitability across a wider range of sectors.

However, stronger earnings alone do not fully explain Japan's market resurgence. A parallel shift in corporate governance, with greater emphasis on shareholder returns and balance-sheet optimisation, has further strengthened investor confidence. These reforms have become a defining feature of Japan's equity revival and are discussed in the next section.

The Third Driver of Japan's Equity Resurgence

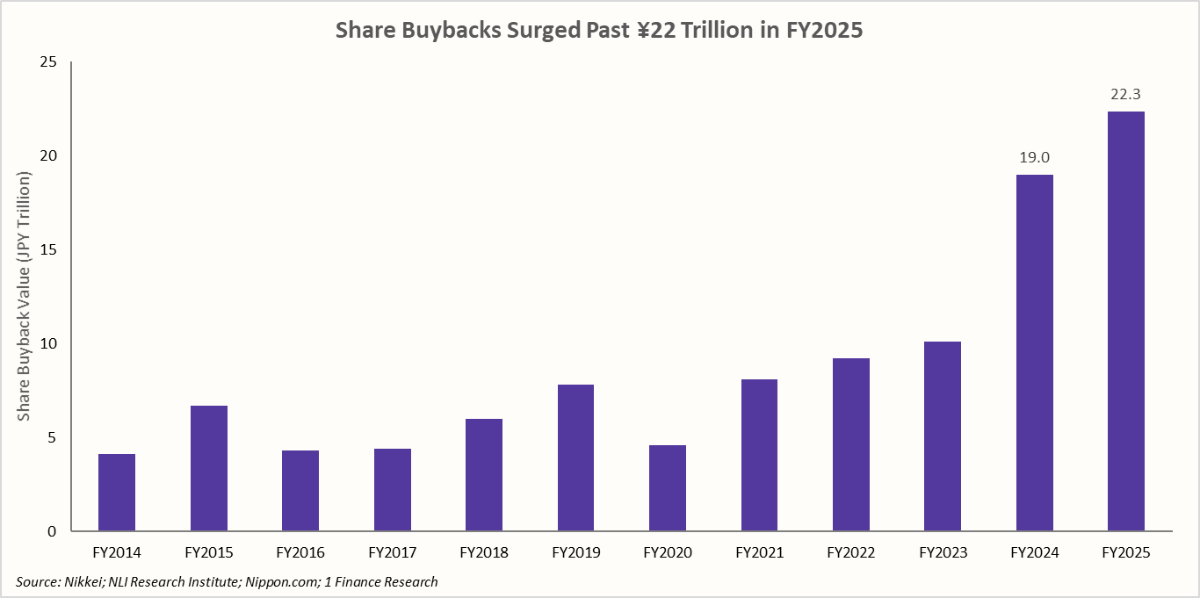

Improving macroeconomic conditions and stronger earnings explain much of Japan's equity rally, but corporate governance reforms are also an equally important structural catalyst. For decades, many Japanese companies accumulated large cash balances and maintained extensive cross-shareholdings, resulting in low capital efficiency, lower return on equity (ROE) and persistent discounts to book value.

To address these inefficiencies, the Tokyo Stock Exchange (TSE) launched a series of governance reforms to improve capital allocation and enhance shareholder value. Companies have responded by raising dividends, accelerating share buybacks, reducing cross-shareholdings and placing greater emphasis on ROE and capital discipline.

The impact is already visible. As the chart shows, announced share buybacks nearly doubled from ¥10.1 trillion in FY2023 to ¥19.0 trillion in FY2024, before reaching a record ¥22.3 trillion in FY2025.

Dividend distributions have also risen steadily, with total cash dividends by listed Japanese companies exceeding ¥20 trillion annually in recent years, reflecting a broader commitment to returning excess capital to shareholders.

For investors, these reforms represent more than better governance. They improve earnings per share, enhance capital discipline and strengthen long-term shareholder returns. Combined with Japan's improving macroeconomic backdrop, they provide a structural foundation for the recent re-rating of Japanese equities, making the current rally fundamentally stronger than previous market recoveries.

Japan's Revival Is Built on Three Stronger Foundations

Japan's equity market resurgence is no longer a story of policy stimulus or a weak Japanese Yen. Instead, it reflects the convergence of three structural shifts: a healthier macroeconomic backdrop, broader corporate earnings, and governance reforms that are reshaping capital allocation. Together, these changes have transformed Japan from a market defined by low returns into one undergoing a gradual structural re-rating.

Looking ahead, H2-2026 is likely to test if the earnings-led performance, rather than mere multiple expansion, drives returns. While GDP growth is expected to remain modest at around 0.8–1.0%, inflation should stay above the Bank of Japan's 2% target, supporting a gradual normalisation of monetary policy.

Another 25 bps rate hike remains plausible in H2-206 if wage settlements stay firm and real incomes continue to improve, reinforcing a virtuous wage‑price dynamic. From here, the durability of the rally will hinge on corporate profitability rather than liquidity alone.

Investors should watch four anchors for earnings: wage trends, BOJ’s policy path, Yen moves and global demand for semiconductors and advanced manufacturing. These will shape revisions to profit expectations through the remainder of 2026.

For Indian investors seeking diversification beyond domestic markets and the US, Japan offers exposure to leading manufacturers, automation, robotics, semiconductor equipment and industrial technology at relatively reasonable valuations versus fundamentals. Governance and capital‑efficiency reforms add a further layer of potential upside.

If reform momentum is sustained, Japan’s narrative may change from demographic constraint to productivity and corporate discipline. That evolution makes Japan less a tactical policy trade and more a strategic allocation within a diversified global equity portfolio.