RBI has removed the interest rate cap on FCNR(B) deposits. NRIs can now lock in FCNR interest rates of up to 7%, the highest this tax-free NRI deposit has offered in years. But the window is short. Fresh deposits must be booked by September 30, 2026, after which this rate structure disappears for every bank.

The change comes from RBI Circular RBI/2026-27/99, which absorbs banks' currency-hedging costs so they can pass the savings on as higher rates, while your money stays parked in its original foreign currency, fully insulated from Rupee depreciation. Here's what changed, why, current bank-by-bank rates, and what to check before you book.

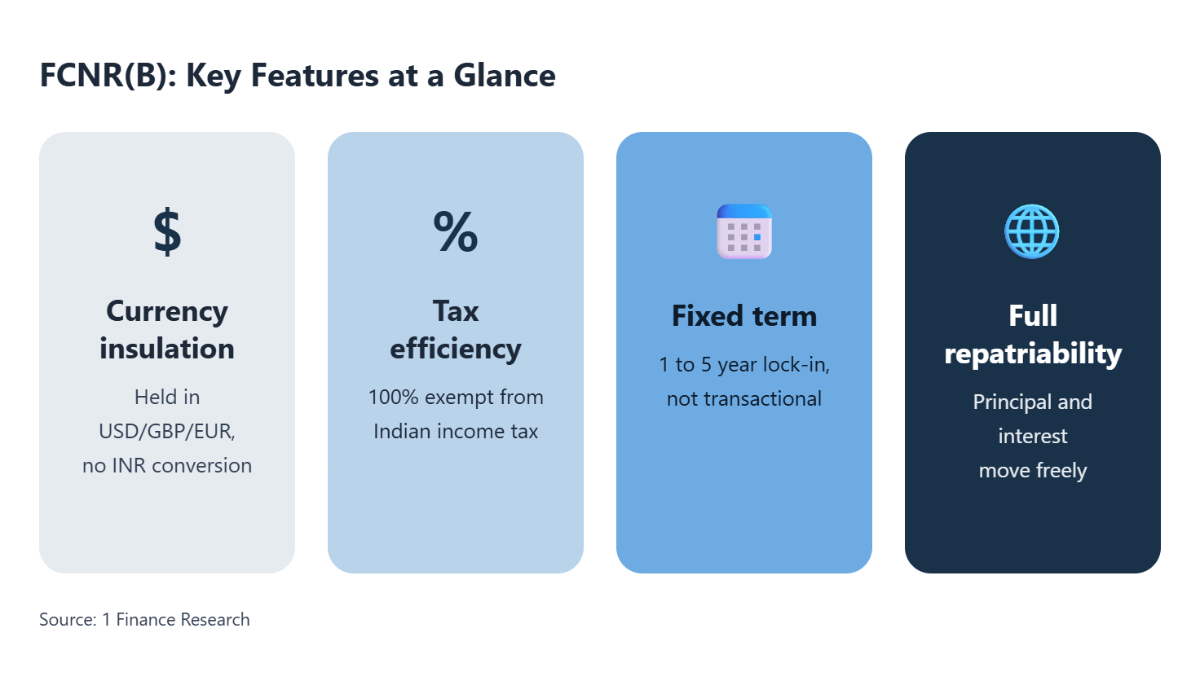

What is an FCNR(B) Deposit?

An FCNR(B) Foreign Currency Non-Resident (Bank) deposit is a fixed-term deposit account built for NRIs and OCIs who want to save in India without converting their money to Rupees. Unlike an NRE or NRO account, an FCNR(B) deposit holds your funds in the original foreign currency, i.e. USD, GBP, EUR, and others for the full term, with zero currency conversion and zero rupee risk.

You lock your funds for 1 to 5 years and earn guaranteed, fixed interest in that same currency, with protection from rupee depreciation for the entire deposit term.

What Changed Under RBI's FCNR(B) Special Window 2026, and why?

On June 8, 2026, the RBI issued Circular RBI/2026-27/99, opening a temporary US Dollar-Rupee swap facility for fresh FCNR(B) deposits. The move is a targeted step to strengthen India's forex reserves and defend the Rupee by pulling in stable, long-term foreign capital, not a routine policy update.

The RBI now absorbs the currency-hedging costs banks normally carry on foreign currency deposits. With that cost gone, banks pass the savings directly to depositors at higher rates, which is exactly why FCNR interest rates jumped to nearly 7% almost overnight.

| What changed before and after the swap window | ||

|---|---|---|

| Feature | Before June 2026 | After June 2026 |

| Eligible Tenure | Standard 1- 5 year range | Strictly 3 - 5 year tenors |

| Hedging Costs | Banks bore these costs (approx. 2.8% - 3%) | Absorbed by the RBI (Zero cost to banks) |

| Interest Rate Caps | Market-linked ceilings | Ceilings removed (enabling 7% yields) |

| Bank Incentive | Limited | High (via CRR/SLR exemptions) |

| Strategic Goal | Standard liquidity management | National Foreign Reserve Defence |

How FCNR 2026 Compares to the Last RBI Swap Window in 2013

The 2026 FCNR(B) swap window isn't a new experiment; it's the same macro-prudential tool the RBI deployed during the 2013 Taper Tantrum, when a similar swap facility helped stop the Rupee's freefall. Understanding what that 2013 window achieved is the clearest way to gauge what this one could deliver.

In 2013, the RBI's swap facility mobilised $34 billion in inflows and added $12 billion to India’s forex reserves, serving as a genuine circuit breaker during a currency crisis, but banks still incurred a 3.5% hedging cost even with the subsidy in place. The 2026 window removes that friction entirely.

| How the 2013 and 2026 Swap Windows Compare | ||

|---|---|---|

| Feature | 2013 Swap Window | 2026 Strategic Window |

| Market Context | Taper Tantrum; Rupee crash | BoP deficit; sustained depreciation pressure |

| Hedging Cost | Implicit/Partial subsidy (capped at 3.5%) | Explicit "Zero-Cost" (fully absorbed by RBI) |

| Inflow Impact | $34 Billion mobilised | $20B - $60B (Estimated) |

| Strategic Result | $12B boost to Forex reserves | Primary shield for Balance of Payments |

| Bank Incentive | Moderate | High (Added benefit of CRR/SLR exemptions) |

With zero-cost hedging this time versus a partial subsidy in 2013, banks have a stronger incentive to pass on rate benefits, which is a core reason analysts expect 2026 inflows to meet or exceed the 2013 benchmark.

Recommended for you

Readers also explored

World GDP Breakdown 2025: Who Powers the Global Economy?

Nifty 50 Companies List 2025 : Top 50 Stocks in India

Comparing FCNR, NRE and NRO Accounts for NRIs

Every NRI managing money in India eventually has to choose between three account types, FCNR(B), NRE, and NRO, and picking wrong can mean paying tax you didn't need to, or losing access to funds when you need them. Here's the difference in one place.

- An NRE account holds Rupee-denominated savings that are fully tax-free and freely repatriable, built for active liquidity, not long-term currency protection.

- An NRO account is for managing income earned within India, like rent, dividends, or a pension, and unlike the other two, it's fully taxable.

- FCNR(B) sits apart from both: it's the only one of the three with zero currency risk, since your money never converts to Rupees at all.

| FCNR(B), NRE and NRO Compared | |||

|---|---|---|---|

| Feature | FCNR(B) | NRE | NRO |

| Currency Risk | None (Held in original currency) | High (Rupee-denominated) | High (Rupee-denominated) |

| Taxation (India) | 100% Tax-Exempt | 100% Tax-Exempt | Taxable (at income slab) |

| Repatriability | Fully & Freely | Fully & Freely | Restricted (requires documentation) |

| Strategic Use | Long-term wealth preservation | Active liquidity for India spend | Managing India - based income |

Which Banks Offer the Best FCNR Deposit Rates in 2026?

FCNR deposit rates currently range from 6.00% to 7.10%, and the gap between banks is wide enough that where you book matters almost as much as when. Smaller Small Finance Banks are pricing aggressively to win NRI deposits, while large private and public banks have converged around a tighter, more conservative range.

| FCNR(B) Interest Rates by Bank and Currency | |||||||

|---|---|---|---|---|---|---|---|

| Bank | USD | AUD | JPY | GBP | EUR | CAD | SGD |

| AU Small Finance Bank | 7.10% | - | - | 4.25% | 2.00% | 3.00% | - |

| Kotak Mahindra Bank | 6-6.15% | 3.85% | - | 3.45% | 1.90% | - | - |

| Punjab National Bank | 6.40% | 5.40% | 0.23% | 6.40% | 4.90% | 4.80% | - |

| HDFC Bank | 6.00% | 6.25% | - | 5.90% | 4.50% | 4.50% | 3.40% |

| ICICI Bank | 6.00% | 6.25% | - | 5.90% | - | 4.50% | 3.40% |

| Axis Bank | 6.00% | 6.25% | 0.01% | 5.90% | 4.50% | 4.50% | - |

| Bank of Baroda | 6.00% | 4.60% | - | 4.60% | 3.50% | 5.00% | - |

| State Bank of India | 3.35% | 4.05% | 0.40% | 3.00% | 1.25% | 2.51% | - |

Source: Respective bank websites (AU Small Finance Bank, Kotak Mahindra Bank, Punjab National Bank, HDFC Bank, ICICI Bank, Axis Bank, Bank of Baroda, State Bank of India), 1 Finance Research

The highest FCNR interest rate isn't automatically the best choice. DICGC insurance covers only ₹5 lakh per depositor per bank, any FCNR balance above that at a smaller bank is an unsecured claim, not a government-backed guarantee. Rates also shift by deposit size and tenor, so treat this table as indicative and confirm directly with the bank before booking.

For larger deposits, prioritise a bank's digital repatriation process over a marginal rate advantage, a seamless transfer at maturity matters more than an extra 0.1% when you're moving six or seven figures.

Understanding FCNR Tax-Free Interest, Yield and Compliance

FCNR(B) interest is 100% tax-exempt in India under Section 10(15)(iv)(fa), but that exemption stops at the border. Your country of residence still taxes this income, and treating the headline rate as your real return is the most common mistake NRIs make with this deposit.

| FCNR Tax Treatment for India and Abroad | ||

|---|---|---|

| Where | Tax Treatment | Notes |

| India | 0%, fully exempt | Applies regardless of deposit size |

| Country of Residence (e.g., US) | Taxable | Reported via FBAR, FATCA, Form 8938 in the US |

Your real return is the after-tax yield, what's left once your home country has taken its share. A 7% FCNR rate can still beat a comparable option like US Treasuries after tax, but only a direct after-tax comparison confirms that, not the headline rate alone.

An FCNR(B) deposit counts as a foreign asset for tax purposes abroad. US-based NRIs must disclose it via FBAR and FATCA; other countries have equivalent rules. Skipping this isn't a minor oversight; non-disclosure penalties are steep.

| Gross Yield (7%) - India Tax (0%) - Home Country Tax (Varies) = Your Net Yield |

| 💡What This Looks Like in Practice Take $100,000 sitting in a 3-year US Treasury note yielding around 4.5%. Moved into a 5-year FCNR(B) deposit at HDFC Bank's current 6% rate, that same $100,000 earns $1,500 more per year, pre-tax. The interest is fully exempt from tax in India, but a US-resident NRI still owes US federal tax on it, just as they would on the Treasury interest. At a 24% federal bracket, the after-tax gap narrows to roughly $1,140 more per year with FCNR, still a meaningful edge, though the exact figure will vary with the depositor's tax bracket and home state. |

What to Check Before the FCNR Deposit Deadline of September 30, 2026

The case for booking now is simple: lock in today's elevated rate for three to five years at a time when global central banks are widely expected to keep cutting rates through 2026 and 2027. This isn't just about catching a temporary spike, it's about securing today's yield before the broader rate environment moves against you.

September 30, 2026 is a regulatory hard stop. Once the window closes, no bank, however aggressive its current rate, can offer these terms on a deposit booked after that date.

| Checks To Run Before Booking An FCNR Deposit | |

|---|---|

| Check | What to Confirm |

| Liquidity | This is a minimum one-year hard lock-in, with the full deposit running three to five years. No interest is paid on withdrawal before year one, and withdrawal after year one is at the bank's discretion, not guaranteed. |

| Global Tax Reality | How to report this deposit at home, through FBAR, FATCA, Form 8938 or a local equivalent. India's exemption does not apply abroad. |

| Insurance Cap | DICGC covers only ₹5 lakh per bank. Split larger sums across banks if this matters. |

| Repatriation | The bank offers a seamless digital process to move funds home at maturity. |

💡 Need liquidity before maturity? Loans or overdrafts against FCNR(B) deposits are a standard feature at most banks, letting depositors access funds without breaking the deposit and forfeiting interest. Loan-to-value limits vary by bank, so confirm the specific percentage and terms with the bank directly before relying on this as a liquidity backstop. |

What This Means for NRIs and Advisors

For NRIs: this window is a rare case where doing nothing has a real cost. If you're holding idle foreign currency savings abroad or have an existing FCNR(B) deposit maturing before September 30, 2026, this is worth acting on now rather than waiting. The rate structure behind this window doesn't survive past the deadline, regardless of what any bank offers afterwards.

For advisors: this is a natural trigger to revisit client portfolios with foreign currency exposure. A few practical starting points:

- Flag clients with FCNR(B) deposits maturing before September 30, 2026 - renewing into the new rate structure before it closes is a straightforward, high-value conversation to initiate proactively.

- Identify clients holding idle foreign currency in regular NRE/NRO accounts or foreign bank accounts who haven't considered FCNR(B). This window makes the case stronger than it's been in years.

- Use the tax-residency angle as a value-add, not just a caveat - walking a client through their actual after-tax yield (India-exempt, but taxable at home) is the kind of concrete, personalised advice that differentiates an advisor from a generic bank pitch.

- Treat the September 30 deadline as a scheduling tool - it gives you a legitimate, time-bound reason to reach out to dormant NRI clients now, rather than waiting for their next scheduled review.