India closed FY26 at 7.7% growth, with Q4 accelerating to 7.8%. The economy benefited from a highly supportive macroeconomic backdrop, including lower interest rates, subdued inflation and fiscal support to households. Many of these tailwinds are likely to be less supportive in FY27.

We expect inflation back above target by October, the rate-cut cycle effectively over, and a below-normal monsoon putting the rural recovery at risk. Growth doesn't fall off a cliff, we still see 6.9% for FY27. But the conditions that made FY26 look easy are reversing, and the year ahead asks harder questions of both the economy and the RBI.

In this edition, we examine the drivers behind India's strong Q4 and FY26 growth performance and assess the outlook for inflation, monetary policy and GDP growth in FY27.

| Section | Key Takeaways |

|---|---|

| GDP Growth in FY26 |

|

| Monsoon Risks and Impact on GVA |

|

| GDP Growth and Inflation Forecast for FY27 |

|

The Growth Drivers Behind India's GDP Surprise

India’s Q4 FY26 GDP numbers reaffirmed the strength of the domestic economy despite a challenging global backdrop. Real GDP growth came in at 7.8% YoY in Q4 FY26, taking full-year FY26 growth to 7.7%, comfortably exceeding earlier projections from several multilateral institutions and private forecasters.

Growth was largely driven by robust activity in the services sector, alongside sustained momentum in construction and infrastructure-related activities. Strong government capital expenditure, improving rural demand, and healthy domestic consumption also provided important support to economic activity during the year.

Overall, the FY26 growth outcome highlights the increasing role of domestic demand as a stabilising force for the Indian economy. The table below presents Gross Value Added (GVA) growth across major sectors and sub-sectors, offering a deeper insight into the key drivers of growth during Q4 FY26 and the full fiscal year.

| Sectors | Q4 FY26 Growth (YoY) | FY26 Growth |

|---|---|---|

| Overall GVA | 7.8% | 7.9% |

| Agriculture, forestry and fishing | 3.6% | 3.0% |

| Industry | 7.3% | 8.5% |

| Construction | 8.4% | 7.4% |

| Mining and quarrying | 5.4% | 5.2% |

| Manufacturing | 7.3% | 10.7% |

| Electricity, gas, water supply & other utility services | 4.1% | 1.7% |

| Services | 9.9% | 9.3% |

| Financial services, real estate and business services | 10.4% | 10.4% |

| Public administration, defence and other services | 5.8% | 5.0% |

| Trade, hotels, transport, communication and broadcasting services | 12.5% | 11.0% |

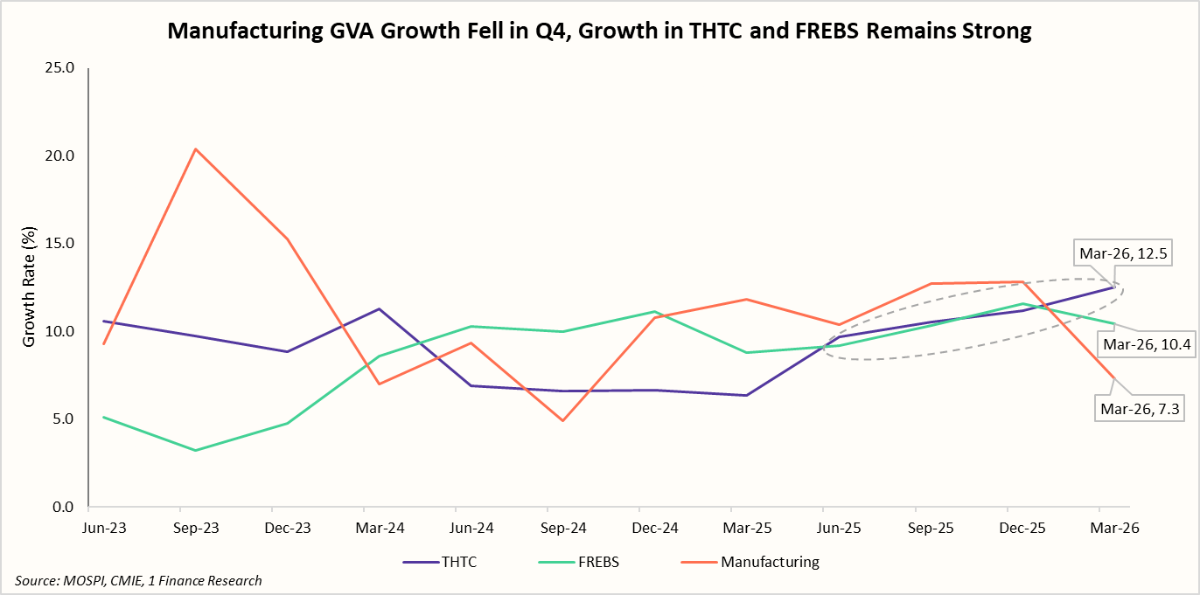

Manufacturing growth moderated to 7.3% YoY in Q4 FY26 from double-digit levels seen earlier in the fiscal year, suggesting a gradual normalisation in industrial activity. In contrast, services-related segments continued to outperform, with Trade, Hotels, Transport and Communication (THTC) growing 12.5% and Financial, Real Estate and Business Services (FREBS) expanding 10.4% in Q4 FY26.

The strength in THTC reflects robust domestic consumption, travel and tourism activity, and increasing formalisation across logistics and communication services. Meanwhile, FREBS continued to benefit from healthy credit growth, rising financialisation of household savings, strong real estate activity, and sustained demand for professional and business services.

Overall, the chart highlights that India's growth is increasingly being driven by the services sector. While manufacturing remains an important pillar of economic growth, services-led expansion remains the key driver of GDP growth, helping offset weakness in external demand and supporting the economy through a period of global uncertainty.

On the expenditure side, growth was mainly driven by Gross Fixed Capital Formation, which surged 11.4% in Q4 FY26, indicating continued strength in infrastructure spending, construction activity, and capacity creation by both the public and private sectors. The sharp improvement in investment demand is encouraging, as it lays the foundation for sustaining medium-term economic growth.

However, Private Final Consumption Expenditure (PFCE) slowed marginally to 7.1%, slowing from 8.2% in Q3-FY26, suggesting normalisation in consumer spending after a strong festive-led pickup. External demand also slowed, with exports slowing down to 3.7% from 5.8% in Q3-FY26, as global uncertainties impacted exports during the period.

Overall, the year FY26 demonstrated the Indian economy's performance, supported by strong domestic demand, services activity and investment-led growth. However, sustaining this momentum in FY27 will depend on several domestic and global factors.

Among the key domestic risks to the FY27 outlook is the monsoon. Recent IMD forecasts point to rainfall deficiencies in several regions, raising concerns over agricultural output. Any significant shortfall in rainfall could weigh on rural demand and food supplies, while also increasing inflationary pressures.

A Below-Normal Monsoon Is the Biggest Risk to FY27

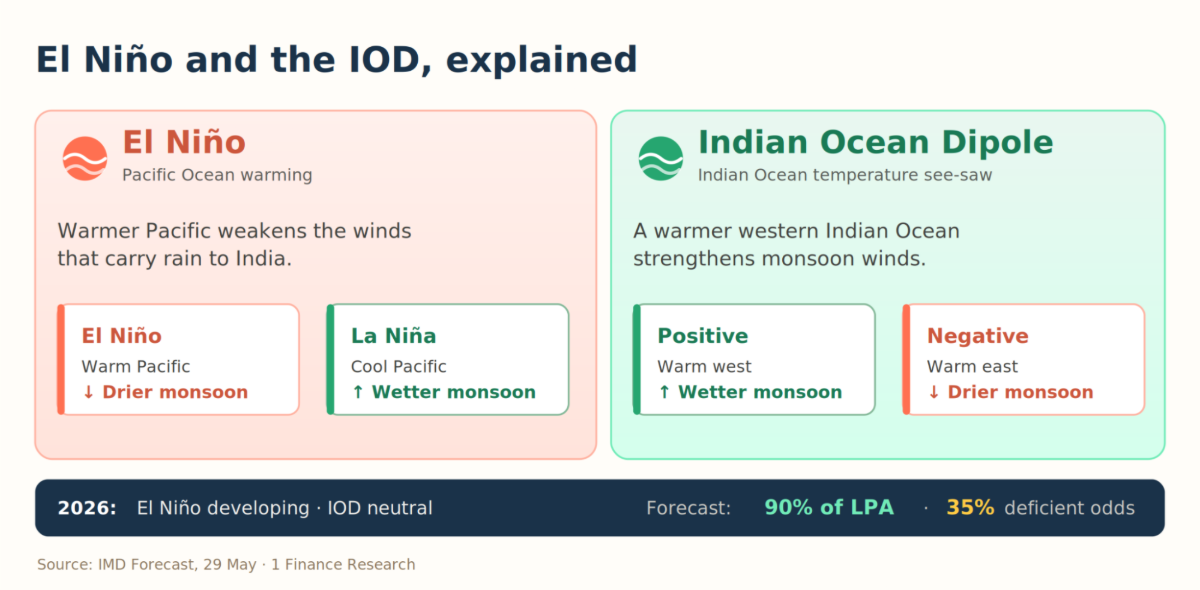

The latest IMD forecast places southwest monsoon rainfall at 90% of the Long Period Average (LPA), indicating a below-normal monsoon season. The outlook is shaped by a developing El Niño, with the Indian Ocean Dipole (IOD) expected to stay neutral through most of the season and turn positive only near its end. The infographic below breaks down how these two ocean drivers pull monsoon rainfall in opposite directions.

The significance of the monsoon extends beyond agriculture's direct contribution to GDP. Although agriculture accounts for around 15% of India's Gross Value Added (GVA), the sector remains a critical source of employment and income for a large share of the population. Consequently, monsoon outcomes have a marked impact on rural demand, food prices and broader macroeconomic conditions.

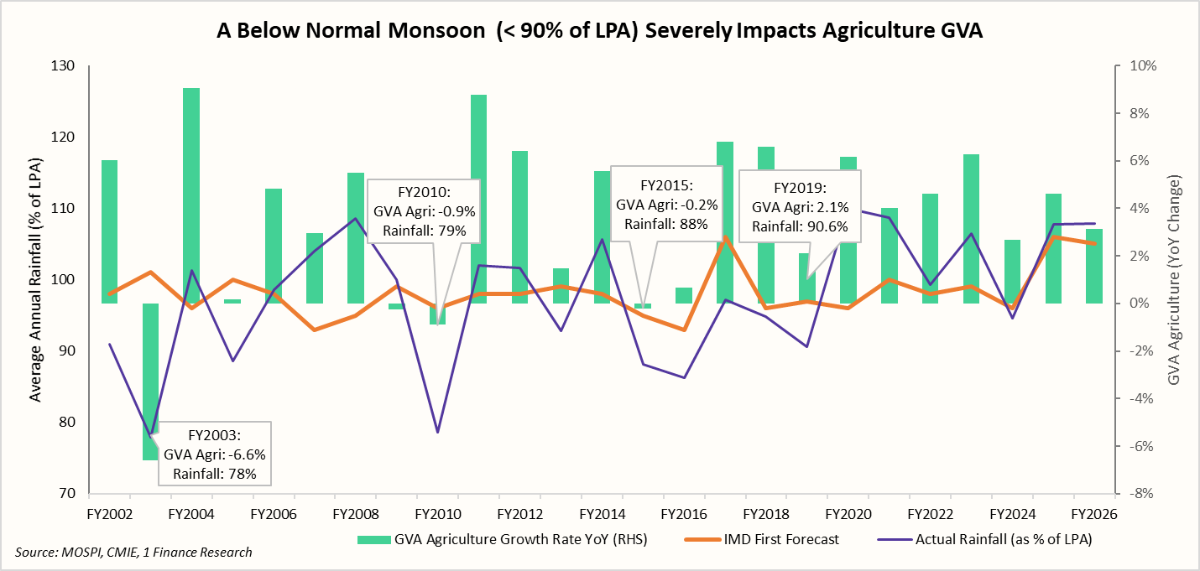

The chart below highlights the relationship between annual rainfall and agricultural growth over the past two decades. The evidence suggests that periods of severe rainfall deficiency have generally coincided with weak agricultural performance. In FY2003, rainfall fell to just 78% of LPA and agricultural GVA contracted by 6.6%.

Similarly, FY2010 and FY2015 witnessed rainfall of 79% and 88% of LPA, respectively, and a sub-zero growth in agricultural GVA. While the relationship is not perfectly linear, agricultural output becomes increasingly vulnerable when rainfall falls materially below normal levels.

The impact of a weak monsoon extends well beyond the farm sector. Lower agricultural production affects rural incomes and consumption, affecting demand for consumer goods, automobiles and housing-related activities. More importantly, a weaker crop season could place upward pressure on food prices, which account for a significant share of India's inflation basket.

Therefore, monsoon developments are closely monitored not only for their impact on growth but also for their implications for inflation and the future path of monetary policy during FY27.

Inflation and GDP Growth Outlook for FY27

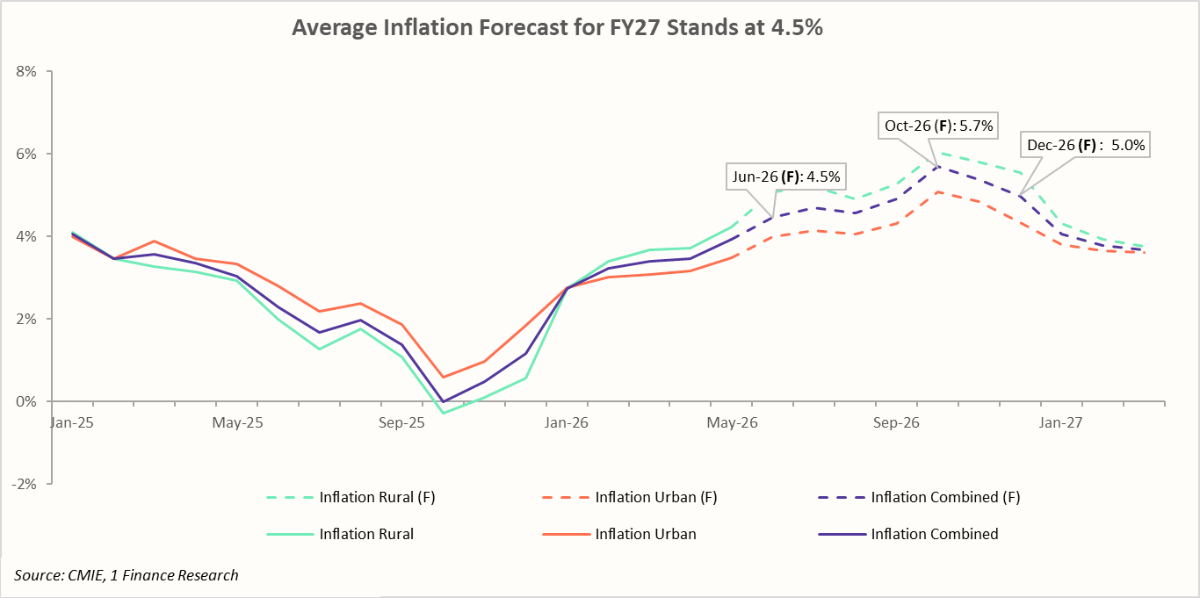

Inflation is expected to re-emerge as a key macroeconomic theme in FY27 after remaining well below the RBI's 4% target through much of FY26. The projected rise reflects a combination of unfavourable base effects and a gradual pick-up in food inflation. As a result, headline CPI is expected to move above the RBI's target during the second half of FY27.

Our forecasts indicate that average CPI inflation could reach 4.5% in FY27, with headline inflation increasing from 3.9% (May-26) to a peak of 5.7% (Oct-26) before moderating towards the year-end. Rural inflation is also expected to exceed urban inflation during much of FY27, unlike FY26, reflecting greater sensitivity to food prices and monsoon-related risks.

As the chart indicates, inflation is expected to remain above the RBI's 4% target through much of H2 FY27, potentially limiting room for further rate cuts. Should inflation approach 5.7% in Oct-26, the policy debate could gradually shift towards the possibility of policy tightening.

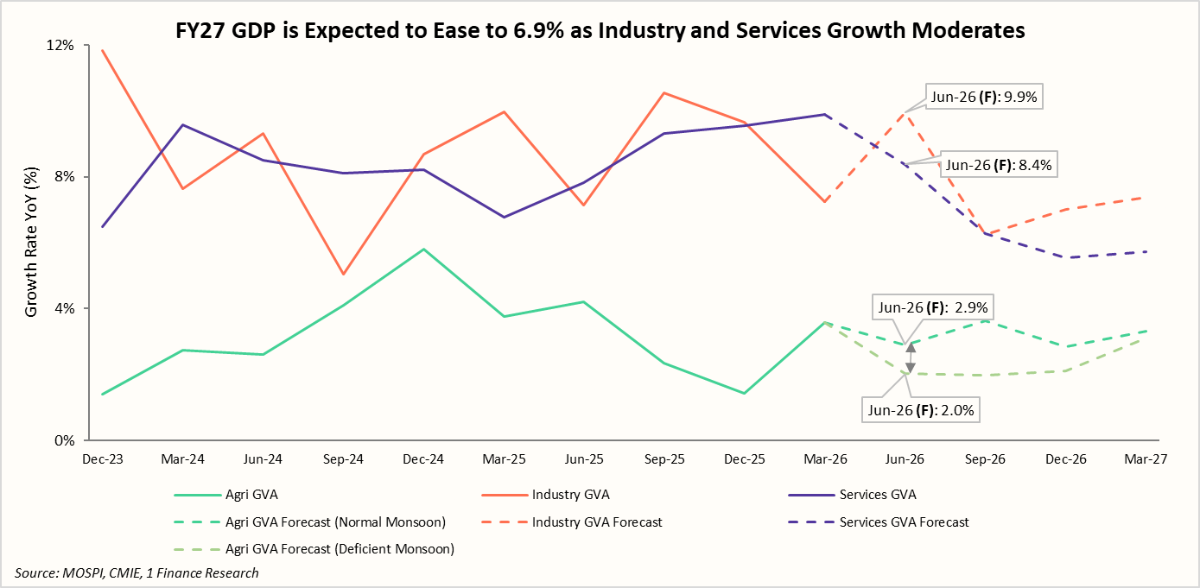

GDP growth in FY27 is forecasted at 6.9% and is expected to moderate from FY26 levels as sector level growth normalises post Sep-26. As the chart below indicates, industry and services growth are expected to ease as favourable base effects fade, although both sectors should continue to remain the primary drivers of economic activity.

Agriculture remains the key source of uncertainty. Under a deficient monsoon scenario (~90% of LPA), agricultural GVA growth is expected to slow by ~0.9% to 2.0% from 2.9% (in the normal monsoon scenario) in Q1-FY27. The impact is likely to be most pronounced in Q2-FY27 (1.6%), which captures the kharif sowing and harvest cycle.

While the effect on headline GDP growth is expected to remain low, a monsoon outcome below 90% of LPA could pose materially larger downside risks to agricultural output, rural demand, inflation and the broader growth outlook.

The Road Ahead for the Indian Economy

India's outlook for FY27 remains constructive, but the growth environment is likely to be more challenging than FY26. Domestic demand, infrastructure spending and services-led growth should buffer the economy against emerging headwinds.

The key domestic risk is the monsoon. Under our deficient-monsoon scenario (~90% of LPA), agricultural GVA growth slows, with the impact most visible in Q2 and Q3 FY27. Agriculture is only ~15% of GVA, but weaker farm incomes could weigh on rural demand for two-wheelers, FMCG and entry-level consumer durables.

However, the broader economy stays supported by strong services (~8.4%) and industrial growth (~7–10%), so overall GDP is expected to moderate only to 6.9%. The bigger challenge may be inflation (FY27 average ~4.5%) rather than growth.

With inflation set to peak near 5.7% around Oct-26, the RBI will have little room to ease. While our base case remains for rates to stay on hold, a sustained rise in food inflation could bring policy tightening back into the RBI's discussion set later in FY27.

On balance, FY27 looks like a year of marginally slower growth, where the risks cluster around prices and the rains rather than the economy itself. Watch the June-to-September rainfall and the inflation it feeds, alongside the US Fed's rate path, as these will shape both market direction and the RBI's next move more than the headline growth number.