In the space of ten days, the UAE has done something no major oil producer has attempted before: challenge both pillars of the post-1974 energy architecture at the same time.

First, it warned Washington that if the Iran war keeps tightening dollar liquidity, it may need to start selling some crude in Chinese yuan. Then, on April 28, it announced its exit from OPEC after nearly six decades of membership, effective May 1.

The yuan warning challenges the currency pillar: the petrodollar system, where Gulf oil is priced and sold in US dollars. The OPEC exit challenges the production pillar: the Saudi-led coordination mechanism that has managed global oil supply for over sixty years.

Neither move is a revolution on its own. The UAE is not abandoning the dollar, and it is not flooding the market with uncoordinated supply. But read together, they signal a country that is no longer content to be a junior partner in either system. It is building optionality on every axis: currency, production, and geopolitical alignment.

| Key Takeaways |

|---|

|

|

|

|

What Actually Happened

During high-level meetings in Washington last week, UAE central bank officials raised the possibility of using yuan or other currencies for oil transactions if the flow of dollars becomes further constrained. They also requested access to a dollar swap line as a financial backstop.

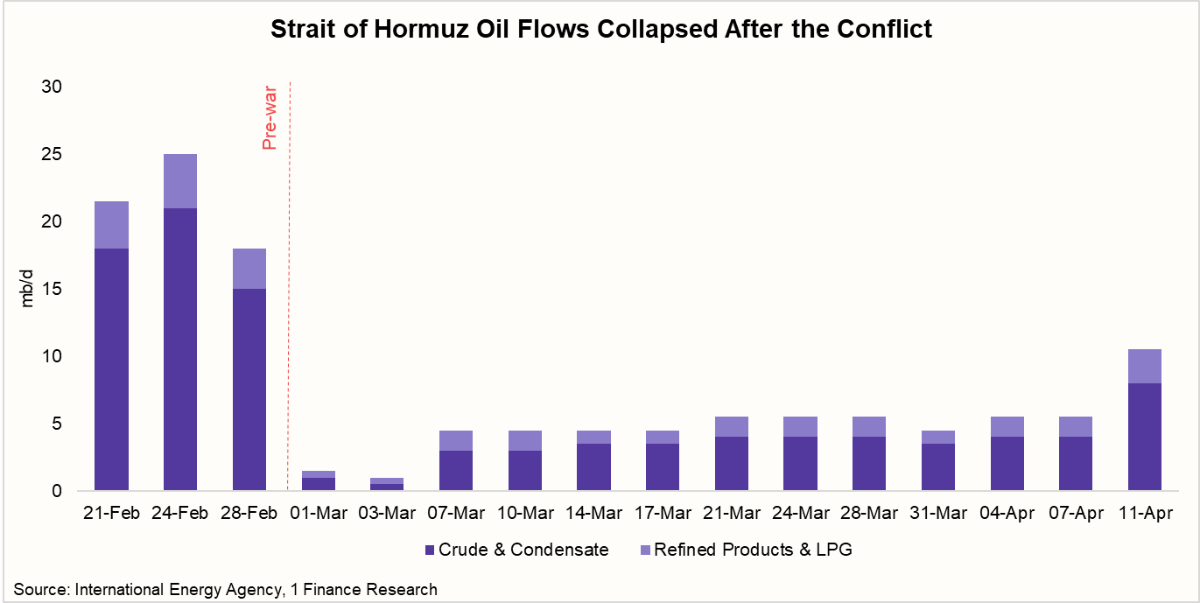

The context is the Iran war and its impact on the Strait of Hormuz. Oil shipments through the Strait have collapsed from over 20 million barrels per day in February to just 3.8 mb/d in early April, choking off the UAE's primary channel for earning dollar revenue. The yuan warning was less "here is our new plan" and more a negotiation tactic combined with genuine risk-hedging. But intent aside, the speed of Washington's public response tells you how seriously this was taken.

Why the UAE Is Worried and How a Dollar Squeeze Forms

The simplest way to understand the UAE's position is this: it is not running out of wealth, but it could run short of usable dollar liquidity if its main channel for earning fresh dollars stays disrupted.

The UAE still holds around $300+ billion in foreign-exchange reserves and manages sovereign wealth assets worth well over $1.5 trillion. This is not a solvency crisis. The risk is operational. Oil exporters earn dollars when they sell crude into global markets. Those inflows support domestic liquidity, reserves, and confidence in currency pegs. When exports are blocked, the economy keeps needing dollars even though fewer fresh dollars are coming in. That is how a country with massive asset holdings can still face a short-term liquidity problem.

| The UAE Is Asset-Rich But Facing a Liquidity Squeeze | ||

|---|---|---|

| Stock (what the UAE holds) | Flow (what has been disrupted) | |

| Foreign reserves | ~$300 billion | Oil export revenue (primary dollar inflow) |

| Sovereign wealth funds | >$2 trillion across ADIA, Mubadala, ADQ | Hormuz shipments down ~80% |

| Dirham peg requirement | Continuous dollar supply needed | Fewer fresh dollars coming in |

This matters because the Emirati dirham is pegged to the US dollar. The central bank must be able to supply dollars on demand to defend the peg and support confidence in the financial system. With Hormuz shipments down roughly 80%, dollar-denominated revenue has collapsed at exactly the moment the economy still needs dollars for imports, debt service, and reserve management.

The yuan option becomes easier to understand in this light. The UAE is not saying the dollar no longer works. It is saying that if dollar access becomes harder during a war-driven trade shock, alternatives become practical rather than theoretical. China already buys roughly 35% of UAE crude exports. Pricing those shipments in yuan would remove an estimated $80 million per day in petrodollar demand, enough to be directionally meaningful for currency markets over months.

Recommended for you

Readers also explored

India's IT Sector Outlook for FY2026

Currency in Circulation: How Much Money Exists in the World?

The Swap Line Is Now the Real Story

The headline-catching part of the story is yuan-priced oil. The more important part is the swap line request.

A swap line is an arrangement between two central banks that allows them to exchange currencies, providing a cheap supply of dollars that can backstop reserves and stabilise a currency peg during periods of market stress. For the UAE, this would not be a bailout. It would be a mechanism to bridge the dollar-liquidity gap until Hormuz shipments normalise.

The calculus is clean:

- If Washington provides the swap line, the UAE stays comfortably inside the dollar system, and the petrodollar architecture holds.

- If it refuses or delays, the conditions for partial yuan settlement become operationally real.

The infrastructure for that shift already exists and is maturing fast. The UAE participates in Project mBridge, a cross‑border CBDC settlement platform with China, Saudi Arabia, Hong Kong, and Thailand. Chinese state banks operate in Abu Dhabi. At least two vessels have already settled Hormuz transit fees in yuan. Saudi Arabia flirted with yuan‑priced LNG in 2023 as leverage during Aramco negotiations—nothing came of it then, but the precedent is there.

The difference now: the UAE’s dollar squeeze is operational, not hypothetical, and the mBridge system is a working multi‑country platform, not a pilot.

| Scenario | Mechanism | Effect on petrodollar |

|---|---|---|

| Swap line granted | UAE gets cheap USD via ESF/ Fed | Petrodollar architecture holds |

| Swap line denied/delayed | UAE must use yuan or other FX | Partial yuan‑priced oil → more non‑USD flows |

| No disruption / normal trade | No need for special arrangements | System reverts to the status quo |

We can expect a meaningful yuan pricing of UAE oil in the next 12 months. But the medium‑term trajectory matters more than the immediate outcome. Every crisis that forces Gulf states to build, test, and normalise non‑dollar payment rails makes the next crisis more likely to trigger an actual shift.

Why the UAE’s OPEC Exit Matters Too

The UAE's decision to leave OPEC and OPEC+ from May 1 adds a second layer to the same story. The UAE has challenged both pillars of the post-1974 oil order: the currency architecture (yuan warning) and the production architecture (OPEC exit). It is not just about payment flexibility anymore; it is also about production flexibility.

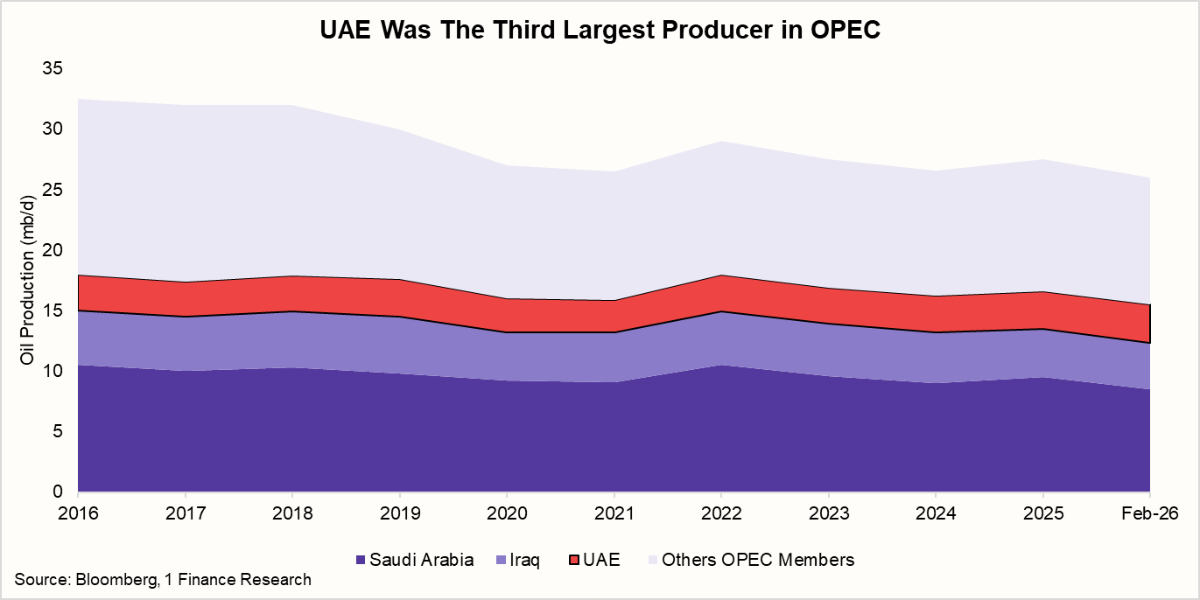

The UAE was the third-largest producer in OPEC behind Saudi Arabia and Iraq, and one of the few members with meaningful spare production capacity. Energy Minister Al Mazrouei framed the decision as opportunistic timing rather than a response to the war. The UAE aims to reach a production capacity of 5 million bpd by 2027 and seeks the freedom to pursue that target without quota constraints.

In the short term, the exit changes nothing. With Hormuz closed, the UAE cannot export at full capacity regardless of OPEC membership. But when the Strait reopens, the UAE plans to pump at maximum capacity without coordination constraints. That is potentially bearish for oil prices over the medium term, which would benefit India's import bill. It also means more price volatility without OPEC's coordination mechanism, which makes hedging harder for importers.

| Impact of the UAE's OPEC Exit on Global Oil Markets | |||

|---|---|---|---|

| Impact Channel | What Changes | Short-Term Effect | Medium-Term Effect |

| OPEC spare capacity | UAE's spare capacity is no longer inside OPEC's coordination framework. | Limited immediate impact while Hormuz remains disrupted. | OPEC loses a major swing producer, making supply management harder. |

| Production competition | UAE can pursue output growth without quota limits. | Little change in the near term. | Greater supply competition could pressure other producers to raise output. |

| Oil price direction | More supply may come from outside the OPEC discipline. | Prices are still being driven mainly by the Iran war and Hormuz risk. | Extra supply could create downward pressure on crude prices. |

| Price volatility | OPEC's role in smoothing supply shocks is weakened. | Volatility stays high because of geopolitical stress. | Volatility may remain elevated without coordinated production cuts or increases. |

| India's import bill | Lower crude prices would help oil importers. | The near-term effect is muted by supply disruptions. | Cheaper crude and more supplier diversification could benefit India later. |

So the UAE is sending two messages at once:

- It wants more flexibility in payments if dollar liquidity tightens.

- It wants more flexibility in production if OPEC discipline becomes too restrictive.

Together, those moves signal a broader fragmentation of the old energy order.

This Is a Petrodollar Warning, Not a Dollar Obituary

That fragmentation raises a bigger question: is the dollar itself losing its grip?

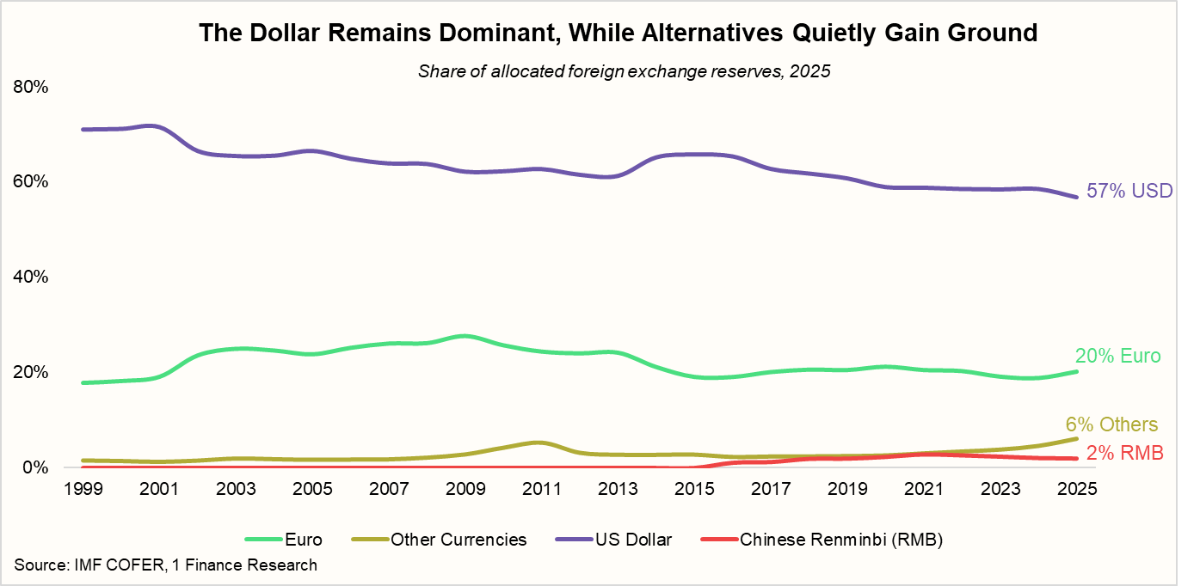

It is tempting to jump from this story to the conclusion that dollar dominance is ending. The broader data does not support that, but it does show a clear direction of travel.

Central banks held around 70% of their reserves in dollars at the turn of the 2000s. By 2025, that figure is closer to 57% according to IMF COFER data. The decline is steady, roughly one percentage point per year, spread across euros, renminbi, gold, and smaller reserve currencies. Gold purchases by central banks are running at the fastest pace in half a century, driven by hedging against the weaponisation of payment systems after the 2022 Russia reserve freeze.

Trade settlement is moving faster than reserves. China and Russia now settle 80-90% of bilateral trade in yuan and ruble corridors. India's Russian crude imports, which nearly doubled to 2.25 million bpd in March, are being settled in rupees, rubles, and dirhams because dollar banking restrictions make USD settlement impractical.

| Bilateral Trade Being Settled in Non-USD Currencies | |||

|---|---|---|---|

| Countries / Corridor | Currencies Used | Primary Goods / Sectors Settled in Non-USD | Details |

| China- Russia | CNY ↔ RUB | Oil, coal, natural gas, machinery, electronics, and agricultural goods | >80–90% of bilateral trade settled in CNY/RUB corridors; energy is the anchor |

| India- UAE | INR ↔ AED | Gold imports, oil re-exports, consumer goods, remittances | System supports trade invoicing + remittance corridor + some energy-linked transactions |

| India- Russia | INR ↔ RUB (plus AED & CNY intermediations) | Crude oil, fertilisers, coal, defence equipment, tea, pharmaceuticals, diamonds | India's Russian oil imports surged, with most paid in INR, ruble, dirham due to USD banking restrictions. |

| Russia- Iran | RUB ↔ CNY + barter | Oil, gas, food, and industrial goods | Both countries bypass USD due to sanctions; barter/pool accounts are common |

But here is the distinction that matters: oil is still priced in dollars even when it is paid for in yuan. Settlement is shifting. The unit of account is not. A shift in settlement does not automatically mean a shift in pricing power, and conflating the two leads to overreaction.

And the data backs this up more clearly than any argument could.

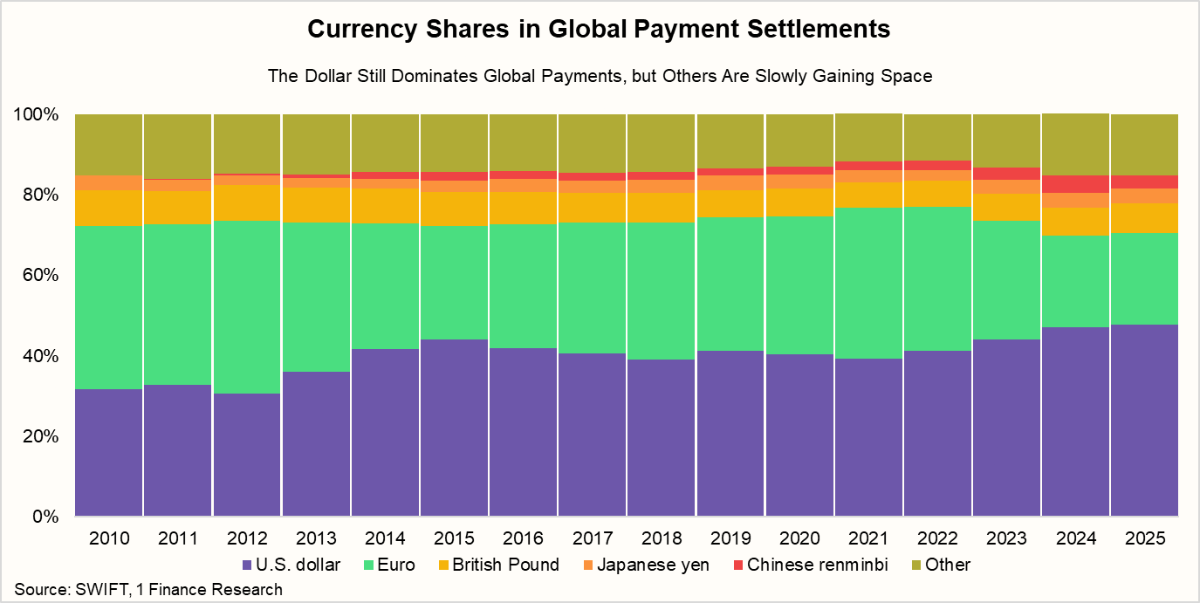

Look at currency shares in global payment settlements over the last 15 years. The dollar hasn't lost ground. It has gained it, rising from around 30% in 2010 to nearly 48% in 2025. The euro, the pound, and the yen are all either flat or shrinking. The Chinese renminbi, despite a decade of active policy push, is still barely visible on the chart.

The petrodollar is bending, not breaking. It is becoming one of several parallel tracks rather than the only one. The UAE's warning tells us that even close US partners now feel comfortable conditioning their dollar reliance on dollar availability, not just political alignment. That is a meaningful shift in posture, even if it never translates into a single yuan-denominated barrel.

What This Means for India

For India, the immediate issue is not whether the world abandons the dollar. The real issue is that India’s oil bill remains tied to a dollar-based system at a time when energy routes, payment channels, and geopolitical alignments are becoming more fluid. That makes India more exposed than many economies to any shock that pushes up crude prices while also tightening dollar liquidity.

The implications should be thought about in four parts:

- The pressure is not just higher oil prices; it is higher crude combined with rupee weakness and tighter dollar funding conditions.

- The inflation impact may appear with a lag, because input-cost pressure usually hits transport, airlines, chemicals, logistics, and fuel-linked categories before it shows up fully in headline CPI.

- A more fragmented oil-settlement system may create flexibility over time, but in the near term, it also makes reserve management and payment architecture more complex for importers such as India.

- The UAE’s exit from OPEC could eventually work in India’s favour by weakening cartel discipline, increasing competition among producers, and putting some downward pressure on global crude prices.

India is therefore neither a passive victim of de-dollarisation nor a natural yuan adopter. It sits in the middle: still highly exposed to the dollar system, but with a strategic interest in building enough multi-currency flexibility to reduce vulnerability over time. At the same time, a looser OPEC structure could give India a modest medium-term benefit if it helps keep oil prices from rising too far.

Looking Ahead

The best framing for this moment is not that the dollar is dying. It is that the petrodollar is becoming less exclusive while the dollar remains structurally dominant. At the same time, the UAE’s exit from OPEC shows that fragmentation is not just happening in payments and settlement, but also in the oil-production framework itself.

The UAE episode is a reminder that the world’s energy-finance architecture is no longer a one-lane highway, even if the dollar still controls the largest and fastest lane. A weaker OPEC means less collective pricing power, more room for independent producer behaviour, and potentially higher volatility in global crude markets. That may not immediately break the price structure, but it does make the system less orderly.

For India, that means watching oil prices, dollar liquidity, OPEC cohesion, and alternative payment arrangements together rather than in isolation. The de-dollarisation trend is not yet a revolution, but it is strong enough that advisors and investors can no longer dismiss it as noise. The deeper shift is not the collapse of one system, but the gradual breakup of the old rules that once kept oil, currency, and supply discipline tightly aligned.