Six months ago, the monetary policy story across major economies was straightforward: inflation was cooling, growth was holding, and central banks were steadily removing the restrictions put in place after the 2022 inflation surge. The Fed cut. The ECB cut. The Bank of England cut. The RBI joined late but cut rates four times. Rate markets were pricing further easing through 2026.

The US-Iran war changed all of that. With the Strait of Hormuz effectively closed since early March 2026, oil above $100 per barrel, and global energy markets in their most severe disruption since the 1970s, central banks that were on a clear easing trajectory are now frozen. The question is no longer how many cuts are coming. It is whether any cuts are coming at all, and for some economies, whether hikes are back on the table.

How Far Each Central Bank Has Come, and Where They Stand Now

The table below tells the full arc of the global easing cycle: where each central bank started, how far it travelled, and where it is now stuck.

| Central Bank | Rate (Current) | Last Change | Total Easing Delivered | Current Stance |

|---|---|---|---|---|

| US Federal Reserve | 3.50%– 3.75% | Dec 2025 (–25 bps) | 175 bps | Hold; 48% probability of zero cuts in 2026 |

| European Central Bank | 2.00% | Jun 2025 (–25 bps) | 200 bps | Hold; hike risk emerging if oil sustained |

| Bank of England | 3.75% | Dec 2025 (–25 bps) | 150 bps | Hold; cuts delayed to H2 2026 at earliest |

| Bank of Japan | 0.75% | Dec 2025 (+25 bps) | +85 bps (hiking) | Tightening; 2 more hikes expected in 2026 |

| Reserve Bank of India | 5.25% | Dec 2025 (–25 bps) | 125 bps | Hold; prolonged pause, hike risk if CPI > 6% |

| People's Bank of China | 1.40% | May 2025 (–10 bps) | 30 bps | Hold; frozen by deflation-inflation squeeze |

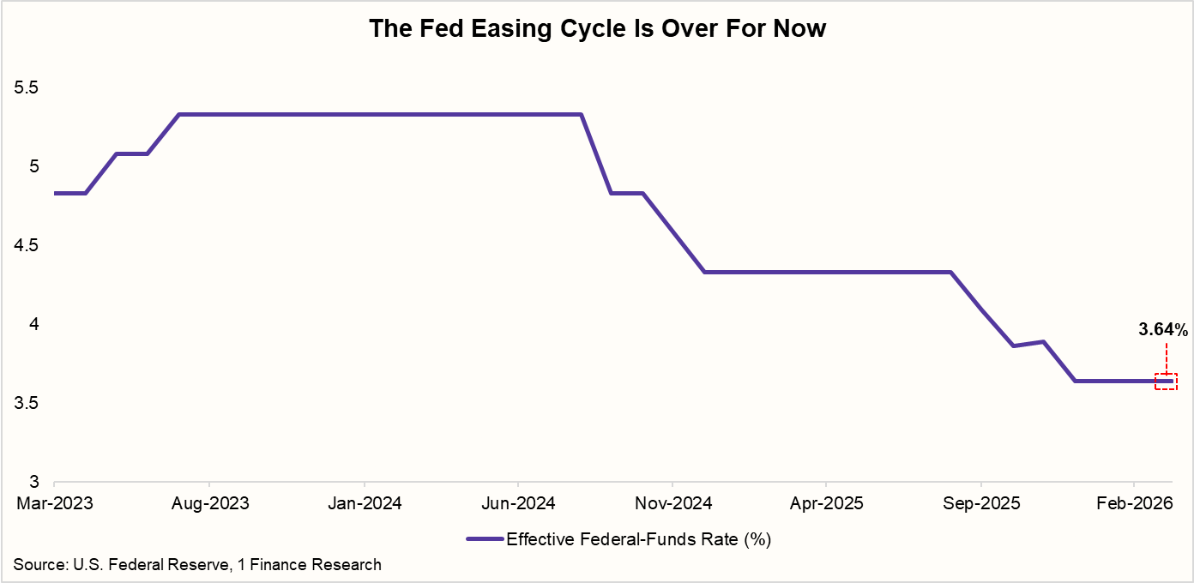

1. The Fed Has Run Out of Road for Now

The Fed delivered 175 basis points of cuts between September 2024 and December 2025, justified on slowing job growth and the assumption that tariff-driven inflation would prove temporary. So it cut.

Then it stopped. The January and March 2026 meetings produced no action, and the March dot plot showed the median FOMC member expecting just one cut across the entire calendar year. More telling: Fed futures markets now imply a median 92% probability of no cut at all in 2026. The shift is entirely attributable to the oil shock.

| Markets See No Fed Cuts in 2026 and a Growing Chance of Hikes | |||

|---|---|---|---|

| Meeting Date | Probabilities | ||

| Ease | No Change | Hike | |

| 29-Apr-26 | 0.0% | 100.0% | 0.0% |

| 17-Jun-26 | 0.0% | 98.1% | 1.9% |

| 29-Jul-26 | 0.0% | 96.0% | 4.0% |

| 16-Sep-26 | 0.0% | 88.9% | 11.1% |

| 28-Oct-26 | 0.0% | 84.0% | 16.0% |

| 09-Dec-26 | 9.0% | 76.6% | 14.4% |

What changed was oil. Core PCE projections for 2026 were revised up to 2.7% at the March meeting, against a 2% target the Fed has been missing for years. Chair Powell gave no indication he was in a hurry. Geopolitical uncertainty, he said, had given policymakers even more reason to wait.

For India, a Fed on hold compresses the interest rate differential between the US and India, reducing the yield incentive for FPI inflows at precisely the moment the rupee is under its sharpest pressure in years.

Recommended for you

Readers also explored

The New Phase for Rates, Liquidity and Inflation

Currency in Circulation: How Much Money Exists in the World?

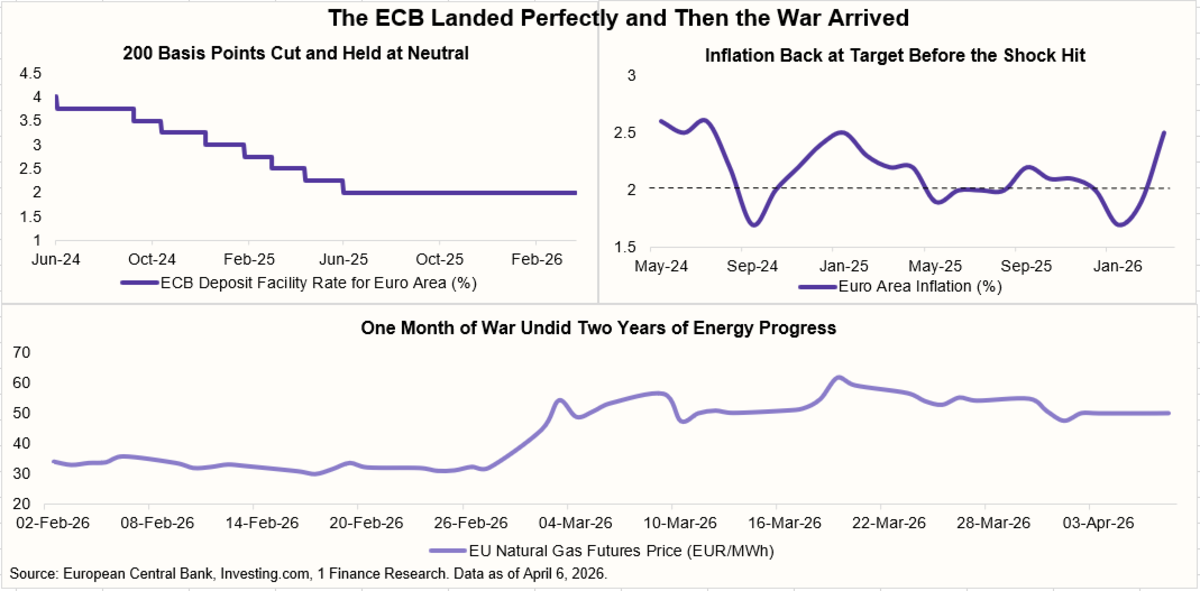

2. The ECB Arrived at Neutral, and Then the War Started

The ECB cut cleanly from 4.00% to 2.00% between June 2024 and June 2025, arriving at what most economists consider the eurozone's neutral rate. By January 2026, inflation had actually dipped to 1.7%, below target, and President Lagarde was describing the eurozone's situation as being "in a good place". The rate-cutting debate was essentially over.

March changed the calculus entirely. European natural gas surged 25% in the days after Iranian strikes on Gulf energy infrastructure. The ECB's 2026 headline inflation forecast jumped to 2.6% from just below 2% in December. High inflation expectations are now pricing in the possibility of ECB rate hikes in the second half of 2026.

The Indian transmission is through trade. A slowing European economy under an energy shock reduces demand for Indian exports in chemicals, engineering goods and textiles.

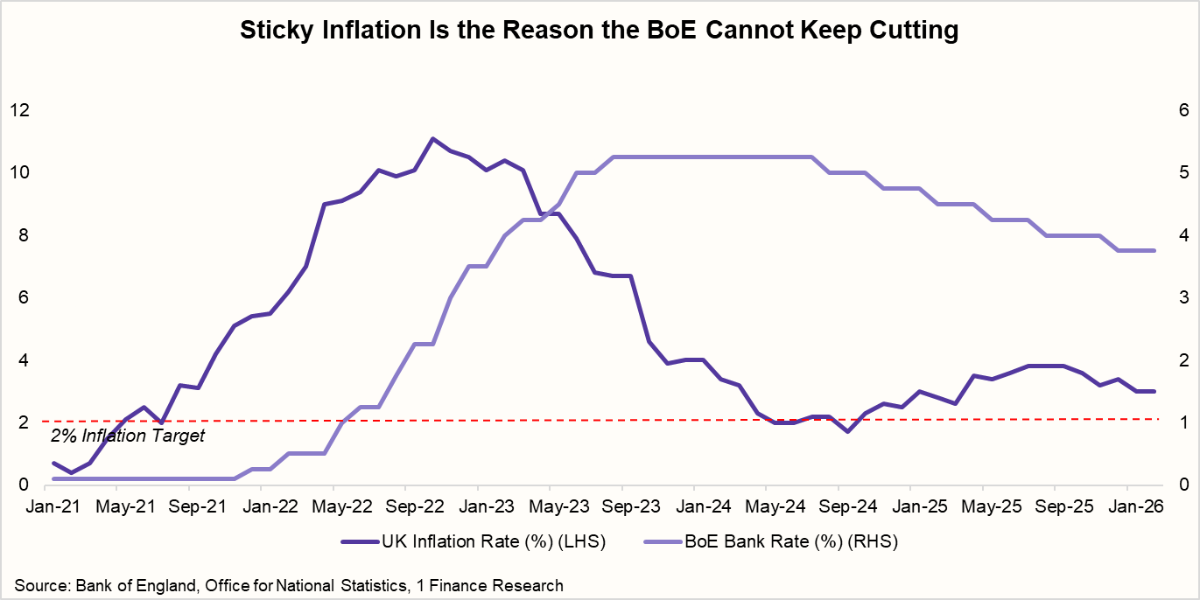

3. The Bank of England Is Caught Between Two Bad Options

The Bank of England is in the most uncomfortable position among G7 central banks right now. It cut rate six times since August 2024, arriving at 3.75%, still the highest benchmark rate in the G7. The war intervened before the next cut could land.

At the March meeting, the BoE held alongside the ECB, with energy costs threatening to push already-sticky UK inflation higher. UK CPI was running at 3% before the shock, unemployment hit a five-year high of 5.2%, and GDP barely stayed positive through Q3 2025. The UK is in the classic stagflationary trap: slowing growth that calls for lower rates, and rising prices that prevent them.

Market pricing has moved decisively against near-term cuts. If energy costs stay elevated through the second half of the year, the first rate reduction is more likely a 2027 story than a 2026 one. The economic data makes the strongest case for cutting, the rate level gives it the most room to cut, and the inflation outlook makes it the least able to act. That contradiction does not resolve until energy does.

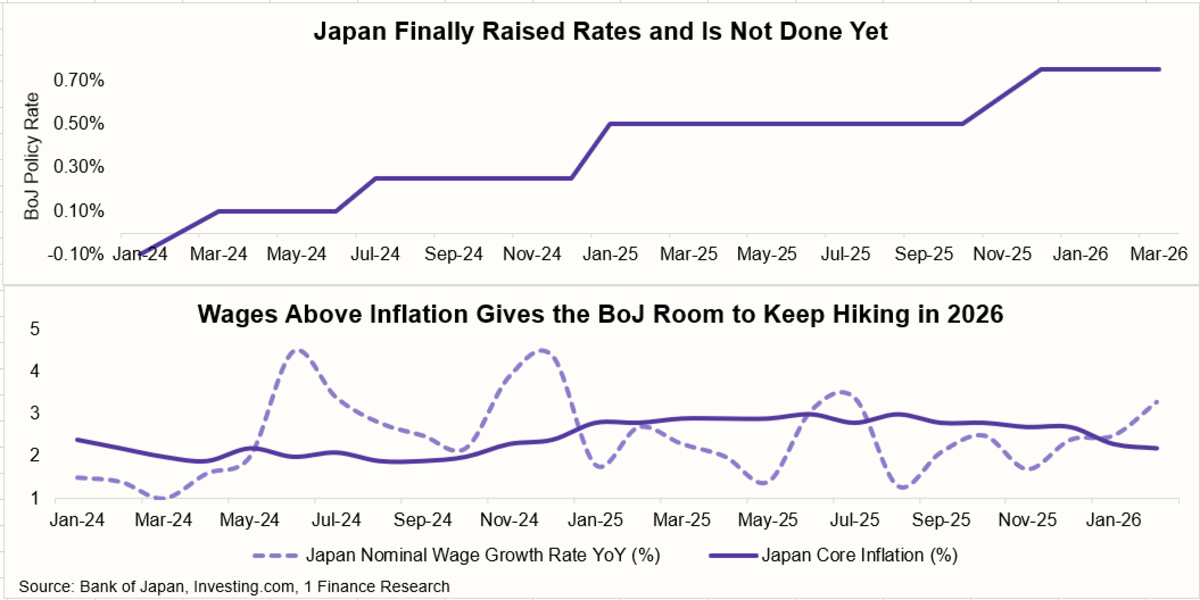

4. Japan Is the Exception That Proves the Rule

While every other major economy has hit pause, the Bank of Japan is moving in the opposite direction. The BoJ raised its policy rate to 0.75% in December 2025, up from –0.10% when its hiking cycle began in March 2024, and two further hikes are expected in 2026.

Japan is tightening because it is finally experiencing the sustained wage-driven inflation its policymakers spent three decades trying to generate. Rising energy costs from the Iran shock have accelerated the inflation trajectory rather than halted it, unlike in economies where inflation was already near target, and policy was in neutral.

For Indian advisors, the BoJ's tightening matters because it determines the cost of the yen carry trade. As Japanese rates rise, the incentive to borrow in yen and invest in higher-yielding markets, including Indian debt, gradually diminishes, adding a structural headwind to FPI debt inflows.

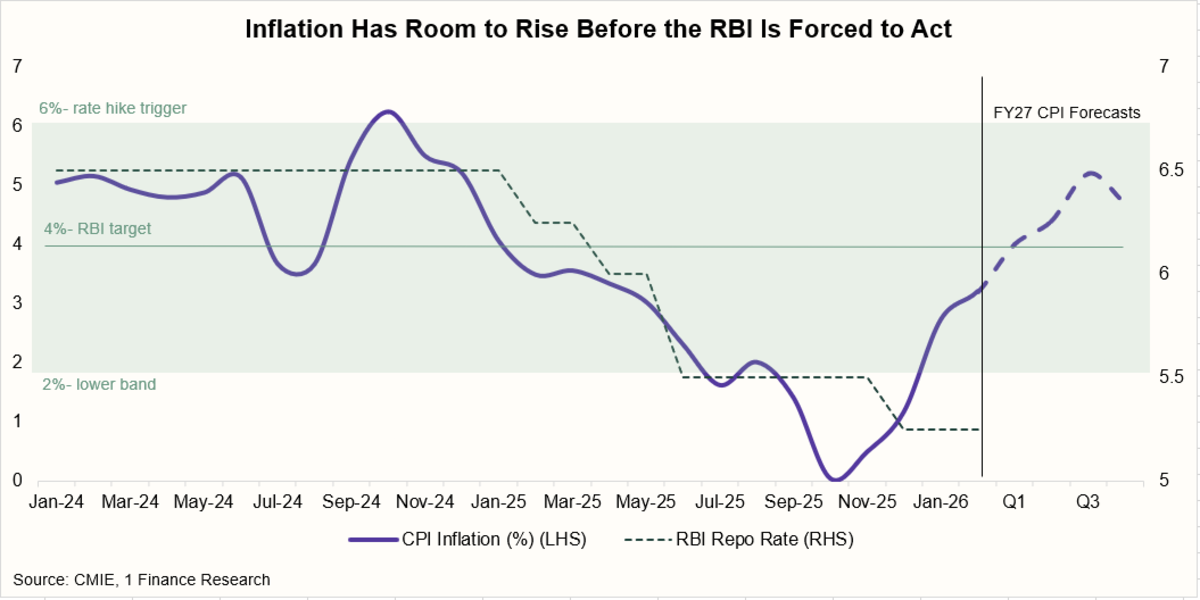

5. The RBI Has Reached the End of Its Cutting Rope

The RBI's easing cycle was late relative to its peers and brief by any measure. After holding the repo rate at 6.50% for well over a year, it began cutting in February 2025 and worked its way down to 5.25% through 125 bps of cumulative reductions.

In its April MPC meeting, the RBI again held the repo rate at 5.25%, a unanimous decision that the market had fully priced in. The neutral stance was retained. The rate decision itself was the least interesting part of what Governor Malhotra said.

The numbers that matter came in the revised forecasts. The RBI has cut its FY27 GDP growth projection to 6.9%, down from 7.4% at the February meeting and sharply below the 7.6% recorded in FY26. The FY27 CPI inflation forecast has been revised up to 4.6%, with core inflation projected at 4.4%.

The MPC's own framing of the situation was telling: “The economy is confronted with a supply shock. It is prudent to wait and watch”.This simply means that the RBI is waiting for external conditions to resolve before it can think about direction again.

So where does the rate trajectory go from here? We see three possible paths.

|

|

|

The 125 bps delivered since February 2025 is almost certainly the full extent of this easing cycle. The question for advisors is not when the next cut comes. It is whether the next move is a cut at all.

6. China Is Frozen for the Opposite Reason

The PBOC is on hold, but not because of the oil shock. Where the Fed, ECB and BoE are frozen because energy costs are pushing inflation up, China is frozen because it was already fighting deflation before the war started. Domestic demand remains sluggish, the property sector has not recovered, and the oil shock has now complicated the deflation fight by raising input costs without generating demand recovery. Beijing cannot cut into rising costs but cannot hold on indefinitely with growth under pressure. The same paralysis arrived at from the opposite direction.

For India, the concern is not the PBOC rate but what Chinese manufacturers do with excess capacity. When domestic demand stays weak, Chinese producers push output into export markets to sustain utilisation, including chemicals, textiles, steel and engineering goods, where Indian exporters compete directly. That is a competitive headwind that monetary policy cannot address.

The Problem No Rate Decision Can Fix

The problem connecting every central bank in this piece is the same: a supply shock that conventional monetary tools cannot fix. Cut into it, and you risk entrenching inflation. Hike into it, and you risk breaking growth that is already fragile. Hold, and you simply wait for external conditions to change. That is where the Fed, ECB, BoE, PBoC and RBI all sit today. Not paralysed by indecision, but constrained by a problem that interest rates were never built to solve.

The Strait of Hormuz is now writing global monetary policy. No rate decision in Washington, Frankfurt, London, Beijing or Mumbai will change that until the physical supply disruption eases. Central banks entered 2026 with the easing cycle almost done and the landing looking soft. They are now navigating something altogether different, and the honest answer is that nobody knows how long it lasts.