For most of FY26, India's macro story was almost too clean. Growth was accelerating, inflation was at multi-year lows, the RBI was cutting rates, and the Union Budget delivered income tax relief without blowing up the fiscal deficit. Then the last quarter arrived and dismantled the assumptions. A West Asia conflict sent crude above $110 per barrel, the rupee hit its worst level since FY12, and foreign portfolio investors pulled out over Rs 1.17 lakh crore in March alone.

The RBI's April MPC, the first of FY27, opened with a GDP forecast revision downward, an inflation forecast that nearly doubled, and language that was materially more cautious than anything the Governor had said in the prior twelve months.

FY27 is not a continuation of FY26. The macro inputs have changed, the risk direction has changed, and the portfolio implications have changed. This edition works through each.

| Key Takeaways |

|---|

|

|

|

|

Inflation Is No Longer Benign

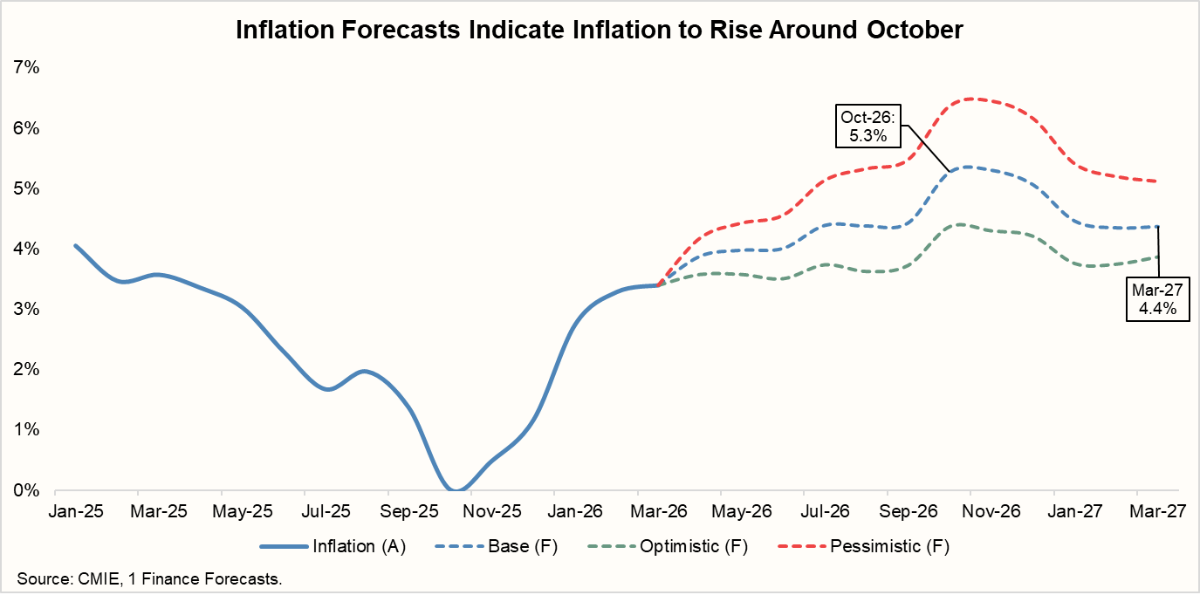

March 2026 CPI came in at 3.40%, the third consecutive monthly rise from 2.75% in January and 3.21% in February due to base effects. Food inflation accelerated to 3.87%. The number came in below market expectations of 3.48% and remains below the RBI's 4% target, providing near-term comfort. What does not change is the direction. March is also the last relatively clean reading before the energy pass-through hits the basket in full.

The RBI's April projections put FY27 headline CPI at 4.6%, more than double that of FY26's 2.1%. The quarterly path climbs: 4.0% in Q1, 4.4% in Q2, peaking at 5.2% in Q3, retreating to 4.7% in Q4. Our 1 Finance estimates corroborate this, with a base case peak of 5.3% in October 2026.

Note: Base case assumes Brent crude stabilises at $90–100 post-ceasefire, the 2026 southwest monsoon at 92% of LPA as per IMD's April forecast, and the rupee in the Rs 92–95 range. The optimistic scenario assumes crude retreats below $85, a normal monsoon, and rupee recovery toward Rs 88–90. Pessimistic scenario assumes crude climbs back above $105, a deficient monsoon, and the rupee depreciating past Rs 97.

Three forces are converging to drive that rise.

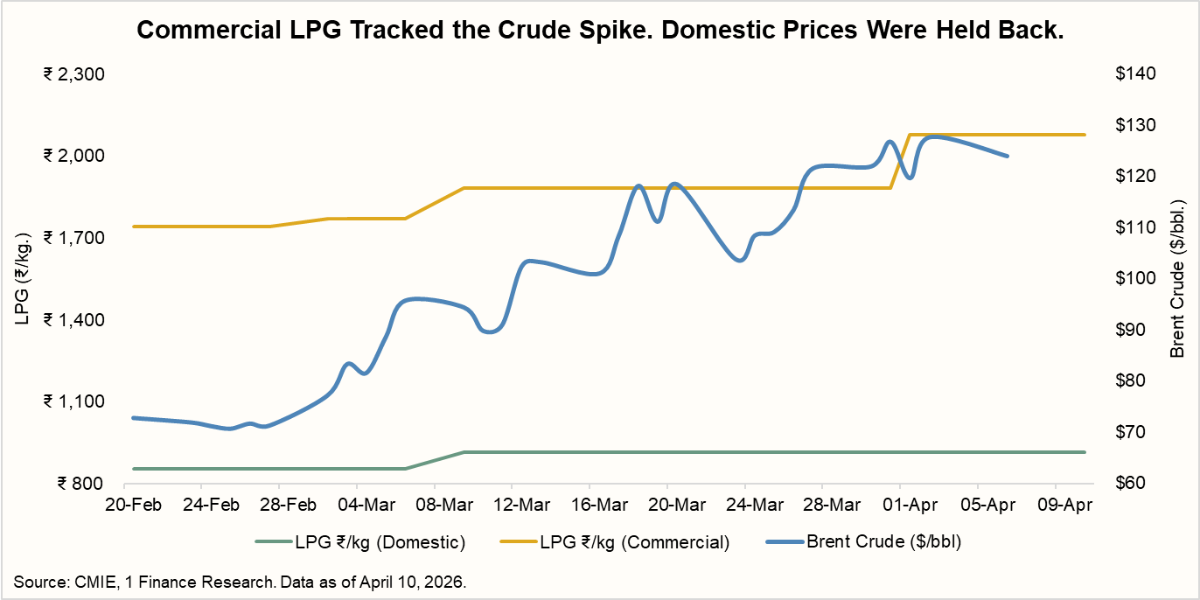

Energy is the most direct. Brent crude crossed $110/barrel following the West Asia conflict, up from $60 to $70 through most of FY25. Every $10/barrel increase adds 0.40-0.60% to India's CPI through fuel costs, freight across supply chains, and manufactured goods inputs. Commercial LPG has been raised twice since March by a combined Rs 310.50 per cylinder. March captured only the first tranche of these increases. April onwards reflects the full quantum.

The rupee compounds the pressure. India pays for crude in dollars, and a currency that depreciated 10.6% in FY26 raises the domestic cost of every imported barrel regardless of international prices. This is persistent, not temporary.

Food is the third risk. The IMD released its official long-range forecast on April 13, projecting 2026 southwest monsoon rainfall at 92% of the Long Period Average, below normal. El Niño is expected to develop during the monsoon season and strengthen through August and September, the exact months when standing kharif crops are at peak water demand.

El Niño episodes typically last nine months or longer, which means the 2027 monsoon could also face suppressed rainfall. Two consecutive below-normal monsoon years would put sustained pressure on food prices well beyond FY27.

Food accounts for 46% of India's CPI basket. With energy already pushing the trajectory upward, a weak monsoon makes the RBI's Q3 peak of 5.2% a floor rather than a ceiling.

The RBI Has Nowhere Left to Cut

The April MPC decision was unanimous: hold at 5.25%, retain the neutral stance. The outcome was expected. The language was not.

In February, Governor Malhotra described the economy as in a "good spot." In April, he enumerated five channels through which the West Asia conflict threatens India's macro outlook: imported inflation, currency depreciation, supply chain disruption, Gulf remittance risk, and investor sentiment.

The 125 bps easing cycle was built on low food inflation, stable energy, and a benign global backdrop. None of those conditions currently holds.

Our Taylor Rule model implies the repo rate should stay near 5.25% under our base case, supporting a pause through most of FY27. Under the pessimistic scenario, however, the model points to 5.50%, requiring one 25 bps hike. Our probability assessment: hold all year 60%, at least one hike 30%, at least one cut 10%. A cut signal only appears if CPI falls durably below 3.9%, which requires the benign scenario to hold fully.

| Probabilities of Rate Cuts in FY27 | Hold 60% Rate stays at 5.25% | Hike 30% +25-50bps | Cut 10% −25 bps |

|---|---|---|---|

| Brent crude | $85–100 post-ceasefire, no re-escalation | Climbs back above $105; conflict resumes | Falls durably below $80; ceasefire holds firmly |

| FY27 CPI | Peaks near 5.0–5.2%, retreats in Q4 | Moves durably above 5.5% through Q3; expectations unanchored | Falls durably below 3.9% for 2+ months |

| Monsoon FY27 | Near-normal; food inflation contained | Deficient; El Niño confirmed; food spikes in Q3 | Above normal; food deflation offsets energy pressure |

| USD/INR | Stabilises at Rs 92–95 | Depreciates past Rs 97; imported inflation compounds | Recovers toward Rs 88–90; FPI flows reverse |

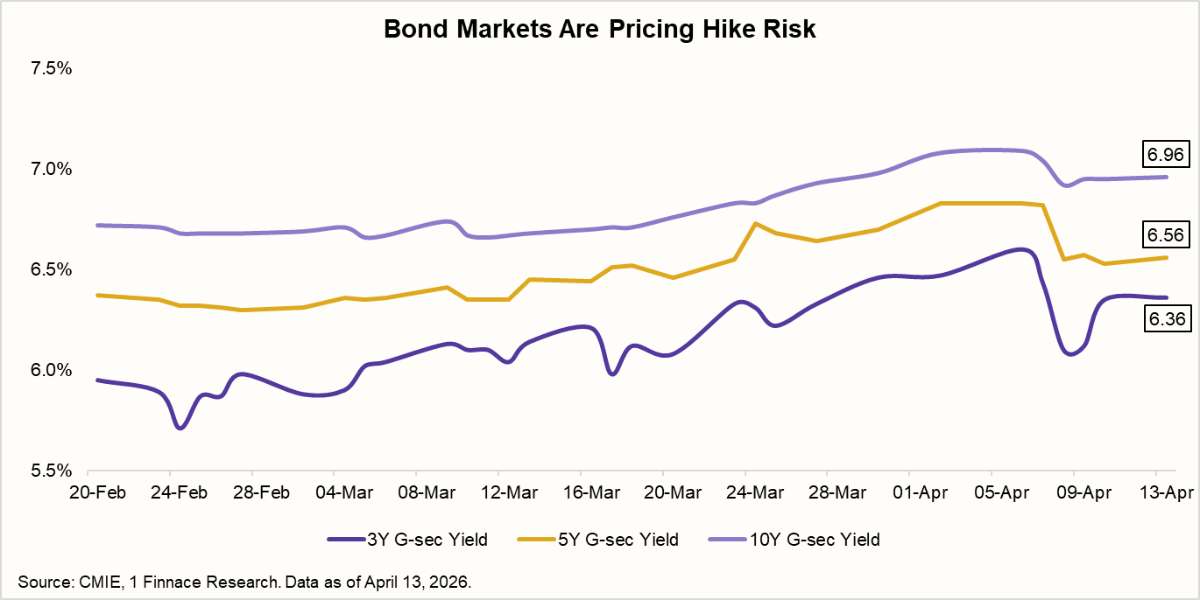

The June MPC meeting is the FY27 inflexion point. March CPI at 3.40% keeps the pause intact for now: it validates the RBI's Q1 projection of 4.0% as credible and removes the near-term trigger for a June hike. But the April CPI numbers, due in May, are the ones to watch. If the energy pass-through arrives in force and April comes in at 4.5% or above, the June meeting becomes a live decision in both directions.

For fixed income, the 10-year G-sec yield has already moved from 6.6% to 6.96% independently of the repo rate, pricing the inflation risk premium. For now, stick to short-medium duration bonds and wait until after the June MPC meeting before adding longer-duration positions. Rate-sensitive sectors, real estate, NBFCs, and floating-rate lending books, should be evaluated assuming rates stay flat for an extended period. The tailwind from last year's cuts has stopped.

The Rupee's Slide Has a Structural Dimension

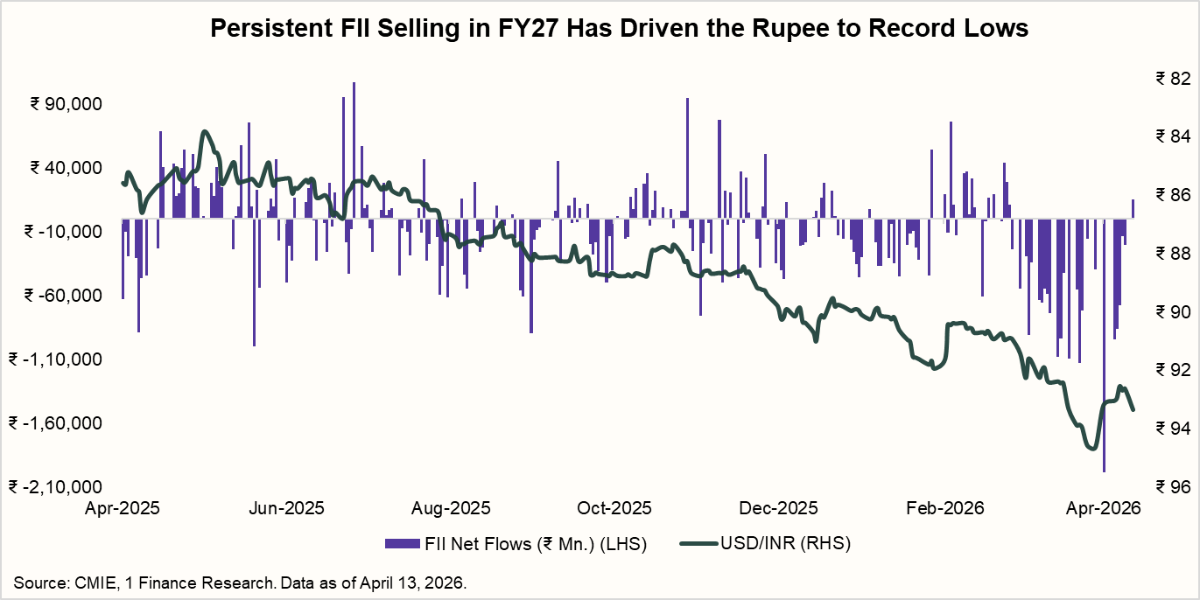

The rupee depreciated 10.6% in FY26, the steepest annual fall since FY12, before closing the year at Rs 95.24. The partial ceasefire relief has brought it back to Rs 93-94, but the forces that drove the slide persist.

The depreciation is built in layers. FPI equity outflows of Rs 1.8 lakh crore in FY26 through mid-April created persistent dollar demand. A widening current account deficit, driven by the oil import bill and elevated gold purchases, compounded the pressure. India's BoP recorded a deficit of $24.4 billion in Q3 FY26; the full year is expected to produce a deficit for the second consecutive financial year. The RBI sold $40 billion in reserves between late February and early April, drawing forex holdings from a record $728 billion down to $688 billion.

In April 2026, the RBI moved beyond intervention and tightened the regulatory perimeter around the rupee. It barred banks and traders from participating in non-deliverable forward (NDF) contracts on the INR in offshore markets, effectively restricting foreign participants' ability to build speculative short positions on the rupee without holding underlying exposure. The move is a signal that the RBI views the offshore NDF market as amplifying rupee volatility beyond what fundamentals justify, and it marks a harder stance on currency speculation than the central bank has taken in recent years.

For advisors, the client conversation is specific. Unhedged international fund holders and gold investors have seen rupee depreciation inflate their FY26 returns. If the rupee recovers, those gains shrink even if the fund's holdings stay flat.

What Advisors Should Do With This

The macro environment entering FY27 is not hostile, but it is no longer forgiving. Three months of rising CPI, a monsoon forecast that puts food inflation squarely in play, and a bond market already pricing hike risk ahead of the RBI mean the FY26 assumptions, that rates would keep falling and that global conditions would remain benign, need to be retired from client conversations. The June MPC meeting is the next hard checkpoint. Till then:

- A part of FY26 returns in international funds and gold came from rupee depreciation, not just asset performance. If the rupee stabilises or strengthens, this tailwind may fade; set the right expectations accordingly.

- Sectors such as real estate, NBFCs, and floating-rate lenders were positioned for further rate cuts. With a pause now as the base case, review allocations against a “rates staying higher for longer” scenario.

- FII outflows of Rs 1.8 lakh crore in calendar 2026 have been the single largest driver of rupee pressure and equity market volatility. For investors looking to add equity exposure, wait for early signs of FII reversal as a more disciplined entry signal.